Our financial lives are mostly a mystery, even to ourselves. As much as we get preached at or lectured at to make a budget, how easily can any of us really recall, from memory, every financial transaction we’ve had in the last six months, six weeks or even six days? And yet that impenetrable cloud of cash, credit, account numbers, confirmation numbers and sometimes checks is the starting point from which financial institutions try to improve our lives, while also earning a profit. Is it any mystery why they’re better at one of those goals than the other?

The U.S. Financial Diaries project is an attempt to penetrate that cloud, using a unique methodology that, while limited in some ways, has a prior track record of transforming the ways policymakers and companies think about how to reach the underbanked.

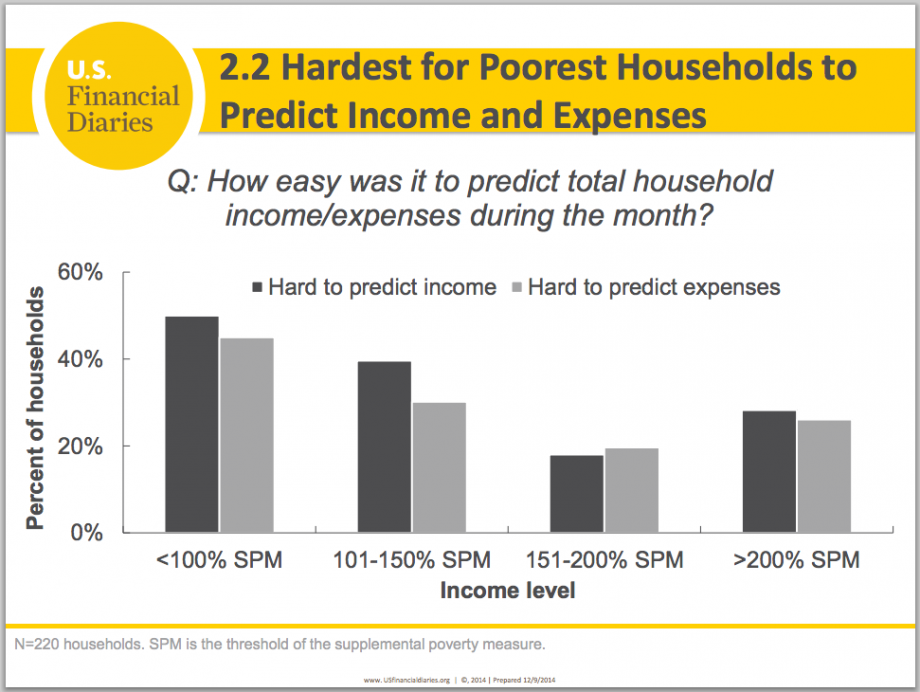

For one year, field researchers from the project visited 235 households (in New York City, around Cincinnati, eastern Mississippi, and south of San Francisco) every two to four weeks and asked them to detail every financial transaction they had — earnings, expenses, savings, debt — in the previous two to four weeks. They ranged fairly evenly from below the federal poverty line to 200 percent above the poverty line.

They wrapped up the diary collection in December 2014, and have since been diving deep into what they found, and they’re starting to share their conclusions. So far, much of their findings can be summed up in one word: volatility.

“The real emergency that families are facing is the short-term dip in income,” says Timothy Ogden, managing director of the Financial Access Initiative, where he oversees the U.S. Financial Diaries project. “Six months a year the households we tracked had income that was either 20 percent above or below their average. So even the concept of average is meaningless.”

The role of short-term savings in coping with income volatility was the subject of new research from the diaries released this summer, neatly summarized in this infographic.

“Most of previous research on financial lives was based on phone surveys, one time, try to get people to recall over a whole year, their financial lives,” Ogden adds. The financial diaries methodology helps overcome the difficulty of remembering every financial transaction over the course of a year. At the same time, researchers develop a deeper level of trust with those they talk to than in a one-off phone survey with a total stranger they’ll never meet.

Ogden recalls a field researcher who told him about a second meeting with one of the households. “He asked them at the end ‘okay are you sure this is everything that’s happened for you financially?’,” Ogden says. “They said yes, he asked a few more times and they said yes, then he says well what about that television that wasn’t here when I was here two weeks ago, and they said, ‘oh we didn’t know you wanted us to tell you stuff like that’ and then they go on for another 45 minutes of stuff along those lines.”

Moreover, Ogden says, “a lot of what’s happening is in informal finance, the sort of financial services that people create for themselves, and that involves loans from friends and family, transactions in cash, things like savings groups and money guards and all kinds of things people do outside of the formal financial system that’s a really big part of how people manage their financial lives.”

The volatility challenges documented in the diaries seem to confirm a finding that earlier researchers could only estimate, that income variability doubled from 1969 to 2004.

(Credit: U.S. Financial Diaries project)

“This is a long-term trend that has largely been under the radar of what’s happened,” Ogden adds. “As a result we haven’t adjusted the way we even think about the problems that these families have, much less develop policies and products for them.”

Inspired by broad research including the diaries, the Center for Financial Services Innovation (also a partner in the diaries project) made coping with income volatility the focus of the first cohort of nine innovators chosen for its Financial Solutions Lab. It’s the first cohort in a five-year, $30 million partnership between CFSI and JP Morgan Chase.

“This is absolutely a solvable problem,” says Ryan Falvey, director of the Financial Solutions Lab. “There’s no shortage of talent, no shortage of investment pouring into the fintech [financial technology] space. What’s missing are the critical tools to help innovative entrepreneurs, for-profit or nonprofit, bring innovations focused on this market to scale and serve millions of consumers. That gap is where the lab now sits.”

Influencing public policy remains an important goal for the Diaries project as well. As just one example, Ogden points to efforts by the AARP to explore policies that would allow companies to build on top of the existing 401k retirement savings infrastructure, giving employees some kind of option or incentive to automatically deduct a small amount of each paycheck into a short-term savings account.

Coincidentally, that is the exact approach currently favored by the Foundation for Louisiana, which, as part of the just-announced City of New Orleans Resilience Strategy, is exploring how to set up emergency savings accounts for low- and moderate-income households. They’re planning to sit down with credit unions, other community groups and companies to figure out how to make it work.

“We were very serious about making sure that the people themselves in our community are better able to respond to and bounce back from a disaster or catastrophe, whether it’s natural, financial or otherwise,” says Flozell Daniels Jr., CEO and president of the Foundation for Louisiana. “The focus would initially be on people who live in vulnerable neighborhoods that would allow them to put away even small amounts of money, five dollars a week, every two weeks. If companies match that one-to-one, it doesn’t take that long to accumulate a few hundred dollars. A few have already expressed to us they’re interested in doing that.”

The Equity Factor is made possible with the support of the Surdna Foundation.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)