When Erik Cole was elected to council in Nashville in 2003, predatory lending was already a hot issue in his district, which included parts of East Nashville.

“My district had a corridor that still has a significant number of … pawn shops and payday loan stores,” says Cole, who also encountered predatory loan cases in his job as executive director of the Tennessee Alliance for Legal Services. “In 2003 when I ran, the biggest comment I heard was, can we not have any more of that in our neighborhood. That was from rich, poor, black, white.”

Cole worked with other council members to pass zoning legislation to restrict new pawn shops, payday lender storefronts, adult bookstores and some other “unsavory businesses,” he says, on that corridor. Unfortunately, Tennessee Quick Cash, a payday lender with one storefront already on the corridor and plans to open a second, successfully sued the city to lift the restrictions. Since then, the city has passed new measures, which payday lenders continue to try to circumvent.

In 2013, Cole left council and became the first director of the city’s Office of Financial Empowerment. In his new capacity, Cole led Nashville’s adoption of the Financial Empowerment Centers (FEC) model, originally pioneered in New York City. The results of that work were published today by the Cities for Financial Empowerment Fund (CFE), the Bloomberg Philanthropies-funded initiative that supports the expansion of the FEC model to other cities.

The centers provide free, professional, one-on-one financial counseling for clients as a public service. Cities bring a local university onboard to train counselors from nonprofits. Nashville partnered with Belmont University and United Way. Counselors are typically embedded, full-time or part-time, at a site where other public services are provided, like welfare or food stamps or community health clinics.

CFE’s newly released findings cover the period from 2013 to 2015. In Nashville, out of 1,708 FEC clients over that period who returned for at least a second visit (allowing the program to track outcomes), 302 clients reduced their debt, 231 increased their credit score, 220 increased their savings, and 175 clients opened or transitioned to a conventional bank account over that period.

Philadelphia, Denver, Lansing and San Antonio also adopted the model. Overall, 5,305 FEC clients across the five cities recorded 14,493 outcomes over the 30-month evaluation period, adding up to a reduction of $22.5 million in cumulative personal debt and an increase of $2.7 million in cumulative saving.

“We found our best integrations were in workforce development and job placement sites, domestic violence shelters, and prison reentry programs,” says Cole.

One of Nashville’s part-time FEC sites was at the Tony Sudekum and J.C. Napier public housing communities, in partnership with a Jobs Plus program site (HUD’s onsite workforce development program that provides a springboard to new careers for public housing residents).

When NYC pioneered the FEC model, it started with just one site, in the Bronx, with private philanthropic support from the insurance industry, including AIG. This was back in 2008, when the company was at the epicenter of the financial crisis. Demand for services was high, which prompted the program to expand to three other NYC sites in 2009, still with only philanthropic funding. After there was evidence of sufficient demand and sufficient quality of services in terms of outcomes for clients, in 2011 the city picked up the bill and scaled up the program, which is now offered at 22 sites around NYC.

The national replications are following suit, with 100 percent private funding for the centers in the first three years. Of 48 cities that expressed interest in the model, five were chosen based on an evaluation of each city’s relationships with local partners and other assets.

“The biggest thing was, who wanted us, what agencies had already identified financial coaching and counseling was an element that could drive good outcomes for them,” says Cole. “NYC’s model was great because we knew where to start, places where benefits were provided, places where case management services happen, where domestic violence intake happens.”

Each city tweaked the model. In Nashville, Cole explains, they had to account for a larger base of homeowners compared to NYC, where a majority of households rent, especially low-income households. They also tracked the household impact of payday lending, which is outlawed in New York state.

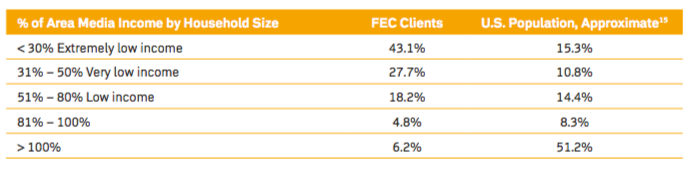

In terms of reach, across the five-city replication, the median monthly income of FEC clients was $1,535, 70.6 percent were women, 62.1 percent had children, and 42 percent were employed full-time (14 percent were employed part-time).

Distribution of FEC client incomes (Credit: Cities for Financial Empowerment)

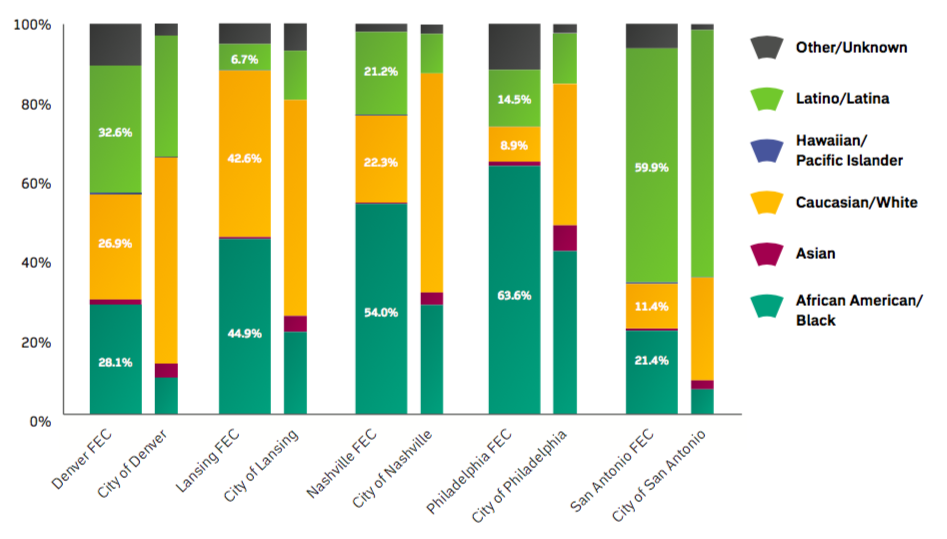

In terms of housing, 53.5 percent of FEC clients were renters, 21.8 percent were homeowners, 12.8 percent reported living with family or friends, 3.4 percent lived in public housing, and 6.5 percent reported being homeless. Nearly 47 percent of FEC clients across the five cities were black, 26.2 percent were Latino, and 17.5 percent were white. Ninety-three percent of clients were U.S. citizens.

Racial and ethnic distribution of FEC clients in city context (Credit: Cities for Financial Empowerment)

Similar to NYC, since CFE’s funding ended, cities have picked up the programs and funded them, in full or in part. Cole still oversees the Nashville effort in his new position as the city’s chief resilience officer. “It’s a natural connection to me to think about what is a person’s personal financial resilience and what is the impact of that on the community,” he says.

The period in which these FEC replications took place has also been a transformative time for the financial empowerment field. New insights and data coming out of the U.S. Financial Diaries Project, especially the publication of The Financial Diaries earlier this year, have dramatically shifted perspectives on how to do this work. Among other insights, the financial diaries research found that for about five months a year, households earned incomes that were either 25 percent higher or lower than their yearly average income.

Other researchers are taking note. Income volatility is the new reality for a majority of American households, according to a Pew study this year that took inspiration from the financial diaries work.

“It is truly transformative for our industry,” says Jonathan Mintz, founding president of CFE. “It’s that granular of a reimagining and understanding of what people are going through and how they really think about getting through not their year, not their month, but their week.”

Mintz, who led the creation and expansion of FECs in NYC as commissioner of the Department of Consumer Affairs under Mayor Michael Bloomberg, gives an example of somebody who has to replace a broken muffler within the next two weeks before the neighbors start complaining. So they save $200 over the next two weeks, but because they had to spend those savings within the same month for a new muffler, the FEC counselor wasn’t capturing that data on monthly or yearly snapshots.

“One of the things that we heard from counselors and that we learned from the financial diaries is, if you take a monthly or yearly snapshot on how somebody builds savings, you’re missing all the energy in between that came and went,” says Mintz.

CFE is now supporting a pilot on top of existing FEC replications in Philadelphia and Nashville to learn what happens when they start to document and support shorter-term savings goals.

“We’re now starting to measure what are your shorter-term savings goals, what are your shorter-term savings successes, and we’re measuring whether we’re capturing a lot of the information we’re missing of effort and success,” says Mintz.

Through the existing FEC client surveys, which also ask questions like how much control do clients feel they have over their own finances, CFE is also trying to measure whether acknowledging the more granular efforts and successes make FEC clients feel more control over their finances.

“In other words, if somebody is feeling like these shorter-term victories are being called out and acknowledged, does that make them feel empowered sooner, and does that make them start investing in these energies more,” says Mintz.

Maybe FEC clients know more about financial literacy than most people give them credit for. Maybe what they need isn’t more information, but more support.

“It’s not that literacy doesn’t matter, it’s that when people are in trouble they need help, they don’t need information,” Mintz adds. “This should not be a box that should be checked off so easily.”

More help is coming. Also today, CFE announced it has opened the application process to replicate the FEC program in 12 more cities or counties.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)