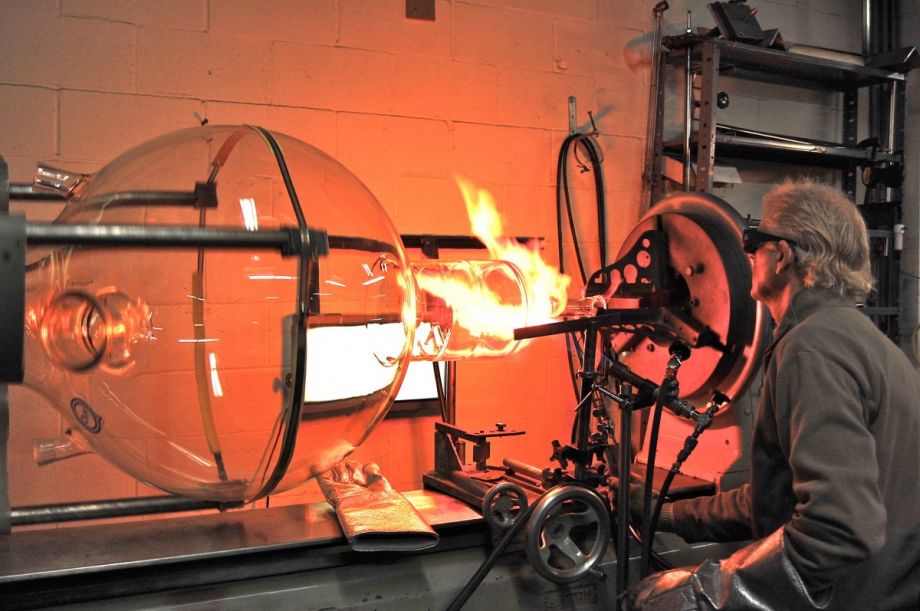

George Chittenden was living his best life in Berkeley, California, as a scientific glass blower — making those condensers, distillers, fermenters, all that intricate and delicate glassware you’ll often find in a sophisticated scientific research lab. It’s a niche business that requires interacting with many clients with very specific needs for highly technical equipment that make scientific discovery possible.

But one day, Chittenden remembers, the owner of the shop where he was working got a cold call from an investor and sold the business. “He was at that point, I guess he was waiting for that cold call,” Chittenden says. “But the [buyer] wasn’t competent, really. There were some really important shortcomings. He just didn’t get it. He didn’t come from this world.”

Over the next three years, morale got worse and worse. A colleague, Tom Adams, asked for a raise and didn’t get it. Adams quit, and it sent Chittenden into a panic. “Tom was the last good thing about that place,” Chittenden says. “And I was concerned for my livelihood. I was committed to the profession, I liked my life, I like being a glassblower, and I was freaking out.”

Chittenden left and joined Adams to start their own scientific glass blowing shop. He borrowed $10,000 from his parents, and Adams did the same. They found some space in the West Berkeley area, protected by the city for industrial use, and opened their doors. That was 1993.

Twenty-six years later, Adams & Chittenden Scientific Glass is thriving: It has clients from all over the world and six employees besides the founders. The pair are still going strong, but they just put a plan in place for when they, too, reach “that point.” With the help of a new collaboration called Accelerate Employee Ownership, the business recently converted into a worker-owned cooperative — and the new employee-owners didn’t have to borrow $10,000 each from their parents.

Chittenden’s not planning on retiring any time soon, but after converting the business to a worker cooperative, he’s excited to share the burden of managing the business among eight people instead of two.

“My most my perfect life would be, you know, to not have so many responsibilities and do more of the stuff that I like, and less of the stuff that I don’t like,” he says.

Accelerate Employee Ownership combines the financial and professional resources of four organizations, two of which are also cooperatives. Project Equity, an Oakland-based nonprofit, is playing the frontline role, including outreach to businesses interested in converting to employee-ownership as well as direct support for businesses before, during and after conversion. Twin Cities-based Shared Capital Cooperative, a cooperatively-run loan fund with 40-years of experience in lending to other cooperatives around the country, is playing the role of financier for the transactions.

The initial funding for Accelerate Employee Ownership comes from the Quality Jobs Fund, a partnership of the New World Foundation and the Federal Home Loan Bank of San Francisco — itself a cooperatively run financial institution owned by other financial institutions in California, Nevada and Arizona. The funding includes $1 million in investment to Project Equity and Shared Capital Cooperative and $4 million to seed a revolving loan fund managed by Shared Capital. Of the loan fund, the majority (close to seventy percent) of the funds will be used to support employee-ownership conversions in the three states in which the Federal Home Loan Bank of San Francisco operates. (The other 30 percent will be used for select national models with a focus on rural areas.)

Accelerate Employee Ownership is one of a few collaboratives or organizations — some national, some local — that are seeking to promote employee ownership as an urgently needed response in the face of 10,000 baby boomers reaching retirement age every day. Analyzing U.S. Census data, Project Equity estimates that baby boomers own half of all privately-owned businesses with employees — that’s 2.34 million businesses earning $5.14 trillion in annual revenue and and paying $949 billion a year in salaries, wages and benefits.

Back in 2013, CNBC reported that as the economy emerged from the Great Recession many baby boomers started taking advantage of optimism in the market to sell their businesses.

It’s a long road to convince city governments or mainstream financial institutions that employee-ownership conversions are worth taxpayer dollars or private investment. Since it was founded in 2014, Project Equity has been laying the groundwork with cities by promoting employee ownership as a strategy for business retention.. Project Equity’s research from the Twin Cities to western North Carolina seem to support this idea: that by putting control of the business into the hands of existing employees, jobs are more likely to stay where they’re located, especially as owners age into retirement.

A Project Equity study of Berkeley found there were 1,200 businesses over 20 years old, accounting for 60 percent of all business revenues in the city ($1.6 billion), and employing one-third of all workers in the city. That study helped convince Berkeley’s Office of Economic Development to enter into a partnership this year with Project Equity.

“Municipal relationships we have found to be a very powerful way to get employee ownership on the menu for businesses,” says Alison Lingane, co-founder of Project Equity. “It matters from the city’s perspective because they care about business retention.”

Besides the benefit of having the city’s stamp of approval on its work, Berkeley’s partnership with Project Equity covers the cost of a feasibility study for interested businesses — the first step toward employee-ownership conversion.

The feasibility study includes an analysis of how much debt the new worker cooperative could possibly take on without endangering the business. A conversion to worker-ownership is typically structured as a sale of the business, from the existing ownership to a new business entity — which may include the existing owners as part of its membership, but it’s still a sale, in which the previous owners do have to agree on a price with the new ownership. That price may require the new business taking out a loan to finance the purchase.

“The way that we position this for the current business owner is, there’s so many multiple inputs that determine what a sale price is, and if you’re going to do an employee ownership transition, the debt capacity analysis tells you what’s the ceiling of an employee ownership transaction,” Lingane says.

Assessing the value of the business is an enormously tricky process, adds Christina Jennings, executive director of Shared Capital Cooperative. “We still see a lot of discussion around how to get to a fair price,” she says. “The selling owner may be depending on this for their retirement, this business is where they’ve had their money invested in many cases. And if in fact it is a profitable and successful business, they should be able to get something out of that.”

Once it’s determined how much the sellers will get out of the conversion, the next question is where will the debt come from. A lot can come from the existing owners, known as seller financing. In an over-simplified example, let’s say the debt capacity analysis says the business can take on $500,000 in debt without being in danger of going under. The seller might choose to finance $250,000 of that — essentially deferring payment of that $250,000 over a period of the next few years. Seller financing is the most flexible kind of financing, and may have zero interest or only enough to keep up with inflation. The good thing is, like in the case of Chittenden and Adams, the sellers often may not want to retire right away, so seller financing can easily cover part of the deal.

“Seller financing has been really critical in nearly all of the conversions that we’ve done,” says Jennings. “There are some projects where the business ends up not wanting or needing outside debt because the seller was willing to provide all the financing, and that’s great because it provides a lot of flexibility for the project — but often that’s not the case.”

Once it’s determined how much seller financing is on the table, the next step is to find any external financing needed to meet the agreed-upon sale price. Project Equity and Shared Capital Cooperative both want local banks or credit unions to be brought into these conversions whenever and wherever possible. Banks or credit unions will generally be able to offer lower interest rates than what they can provide, even through this new collaborative. The ultimate vision is for employee ownership conversion loans to become as normal a business lending product as any other for mainstream banks and credit unions — but there are still plenty of barriers, starting with the lack of familiarity with worker cooperatives in particular.

“It is a different beat,” Lingane says. “How do you think about a business that has 20 owners instead of one or two or three or maybe five? Over five, it doesn’t fit into the boxes of how lenders do things.”

Collateral requirements are also a barrier. Sometimes, Jennings says, if the business owns its building or other significant assets like valuable equipment or maybe vehicles, it’s possible to use that as collateral to get a bank or credit union comfortable making a loan that might cover at least part of the external debt needed to finance an employee-ownership conversion.

“But a lot of what we’ve seen is a more general transfer of assets and limited equipment and working capital and that’s not something a typical bank is able to finance,” says Jennings.

Only after looking into any external financing does Shared Capital step in with a loan or investment of its own. Sometimes, Jennings says, other lenders may want to see Shared Capital commit some external financing first, and only then are they comfortable financing part of an employee-ownership conversion.

“Success for us means those lenders are willing to start coming into these projects without us having to bring them in,” Jennings says.

For now, the Accelerate Employee Ownership collaborative members are excited to solve each other’s bottlenecks. For Project Equity, it’s having a ready access to a financial institution with the same commitment to employee ownership as it does, not to mention a 40-year track record of lending to cooperatives. For Shared Capital Cooperative, it’s having an on-the-ground presence as Project Equity is building in various locales to build up a pipeline of employee-ownership conversions — in addition to Berkeley, Project Equity also recently launched a formal partnership in Long Beach, California, where it held the kickoff event for the collaborative. It’s also important to Shared Capital Cooperative that businesses get support after the formal transition, as they get used to sharing management and business decision-making among equals — and Project Equity provides that support as well for up to two years post-transition.

Accelerate Employee Ownership has already supported two conversions so far: Adams and Chittenden’s glass-blowing shop and California Solar Electric, a solar design and installation business located in rural Grass Valley, California.

“We will be raising more funds to be able to support the financing of transitions nationally through this collaborative,” Lingane says. “We’re finding cities are really excited that we can step in with a whole program, and also it’s not just about business retention but it can also be about their equity goals.”

While they are open to any business that approaches them about converting to 100-percent employee ownership, Lingane says the collaborative will focus outreach on sectors known for low-wage work, in line with both Project Equity and Shared Capital Cooperative’s existing goals. “Unfortunately in our economy if you do the Venn diagram of people in lower-wage jobs and people of color, in our urban environments especially, there’s a big overlap there,” says Lingane.

It’s also the main goal of the Quality Jobs Fund to support initiatives and organizations that focus on supporting businesses that offer living wage jobs with benefits, on the basis that such jobs ultimately allow more families to become homeowners.

“For employee ownership to become less of a fringe and more of a mainstream thing, I think these are all pieces of that,” Lingane says.

UPDATE: After receiving clarifying information from New World Foundation, we’ve clarified that the $1 million from the Quality Jobs Fund is an investment, not a grant, and that the revolving fund is not required to make 70 percent of its loans in California, Nevada and Arizona, but is targeting that share nonetheless.

This article is part of The Bottom Line, a series exploring scalable solutions for problems related to affordability, inclusive economic growth and access to capital. Click here to subscribe to our Bottom Line newsletter.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)