In the depths of the Great Depression, the nation’s leaders identified homeownership as a way to kick-start the nation’s economy by creating community-based wealth. It took them years of trial and error, but they eventually constructed a vast, multifaceted system to build community wealth, homeowner-by-homeowner.

In 1932, they created the Federal Home Loan Bank system, which makes cheap capital available for consumer lenders to take and turn around and make relatively inexpensive loans to borrowers. In 1934, they created the Federal Housing Administration (FHA), which insures loans made by banks and other private lenders for home building, giving them a measure of government-sponsored protection against the risk of making millions of relatively small loans. Then in 1938, they created the Federal National Mortgage Association. More commonly known as Fannie Mae, it buys mortgages from lenders, giving them the cash to continue making more loans instead of waiting till loans got paid back in order to keep growing.

These three institutions provided the foundation for creating wealth at the family and community level for millions of people — but only if they were white.

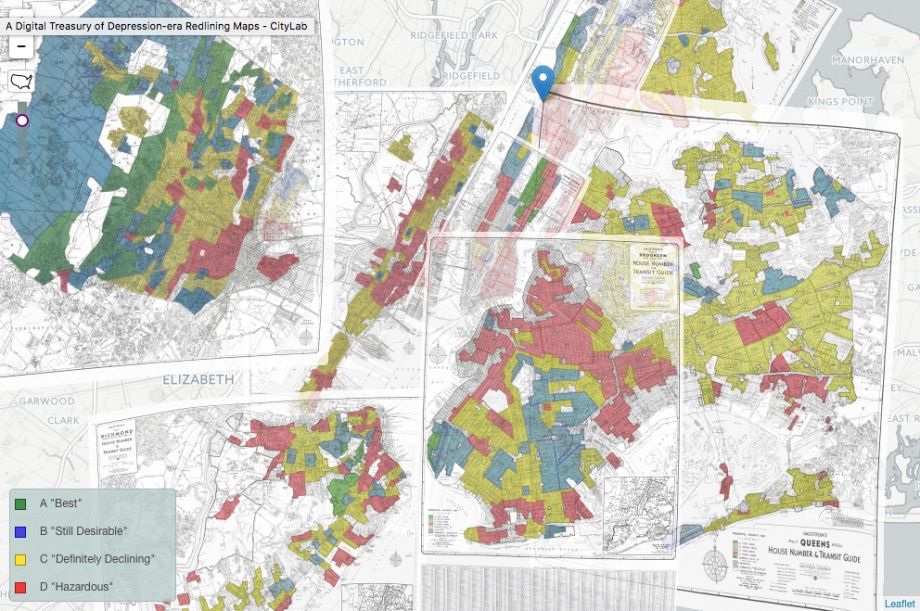

Now, thanks to researchers at the University of Richmond, the historic maps that guided the wealth creation machine created in the 1930s are now more accessible than ever before, in a platform called “Mapping Inequality: Redlining in New Deal America.”

Mapping Inequality provides interactive access to a collection of 150 “security maps” and 5,000 accompanying area descriptions produced between 1935 and 1940. These infamous maps and descriptions illustrate how the great government-backed wealth-creation machine of the 1930s only worked for white people.

The maps were the work of the Home Owners’ Loan Corporation (HOLC), a subsidiary of the Federal Home Loan Bank system. Until now, the maps and descriptions have really only been available to people with access to deep historical archives, or occasionally made an appearance online.

HOLC solved an immediate issue: how to determine the risk of making a specific loan. There were no credit agencies or ratings at the time, so HOLC hired mortgage lenders, developers and real estate appraisers in nearly 250 cities to create maps that color-coded neighborhoods and entire cities based on assessed risk. HOLC assessors looked at a number of factors, including housing stock, proximity to factories or docks, or positive influences like city facilities or parks.

But as many scholars who have studied these maps and descriptions have shown, the factor that assessors most associated with the highest risk is a high percentage of “negro” population. HOLC maps overlay or outline the riskiest neighborhoods in red, which is where the term “redlining” comes from. Conventional banks and most other lenders denied loans to purchase or rehabilitate property in redlined areas.

Harlem, despite being at the tail end of the Harlem Renaissance, was completely redlined. The HOLC area description for Harlem reads: “Formerly a good residential district with many well built private homes. Now practically entirely negro with many tenements.” In Brooklyn, the HOLC description for Bed-Stuy reads: “Colored infiltration a definitely adverse influence on neighborhood desirability although Negroes will buy properties at fair prices and usually rent rooms.” Many of Chicago’s redlined area descriptions are extensive, almost essay-like, detailing the patterns of racial and also immigrant presence.

It’s not just the big major cities, either. Pennsylvania’s Altoona and Johnstown, Indiana’s Muncie, Alabama’s Birmingham and Montgomery, California’s Fresno and Stockton are all among the mix on Mapping Inequality.

The wealth creation machine created in the 1930s worked brilliantly for some, and not at all for others. The pattern has never been more clear.

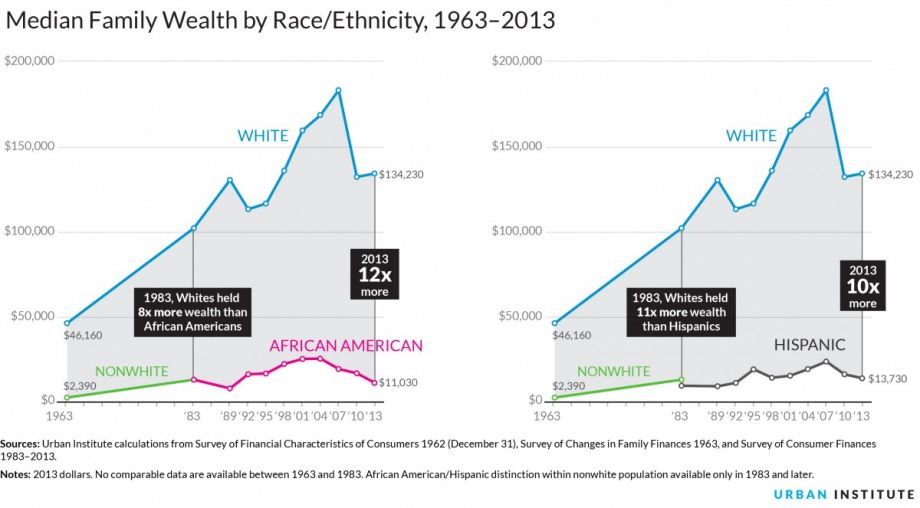

(Credit: Urban Institute)

Redlining wasn’t officially reversed as a federal policy until the Fair Housing Act of 1968. By that point, it had infused its way through out the entire mainstream consumer banking system, as mortgage lenders set the standards for the whole industry. The Community Reinvestment Act of 1977 finally made redlining illegal across the entire banking system, and also established the obligation of banks to show they are meeting all the credit needs of the communities where they do business.

Communities are still fighting today to reverse the legacy of redlining. It’s only been around 20 years since the federal government officially recognized community development financial institutions (CDFIs), many of which emerged specifically to provide access to capital in formerly redlined neighborhoods.

Perhaps the great government-backed wealth-creation machine is turning a corner: Since they were first permitted to become members in 2008, at least 40 CDFIs have become members of their regional Federal Home Loan Bank branch.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)