In 1998, Cesiah Toro Mullane and a group of her neighbors testified before the Federal Reserve Board of Governors. They were part of a small group of activists, small business owners and other residents of Brooklyn Community District 5 who started meeting in the mid-1980s to discuss how to get local banks to lend in their neighborhoods.

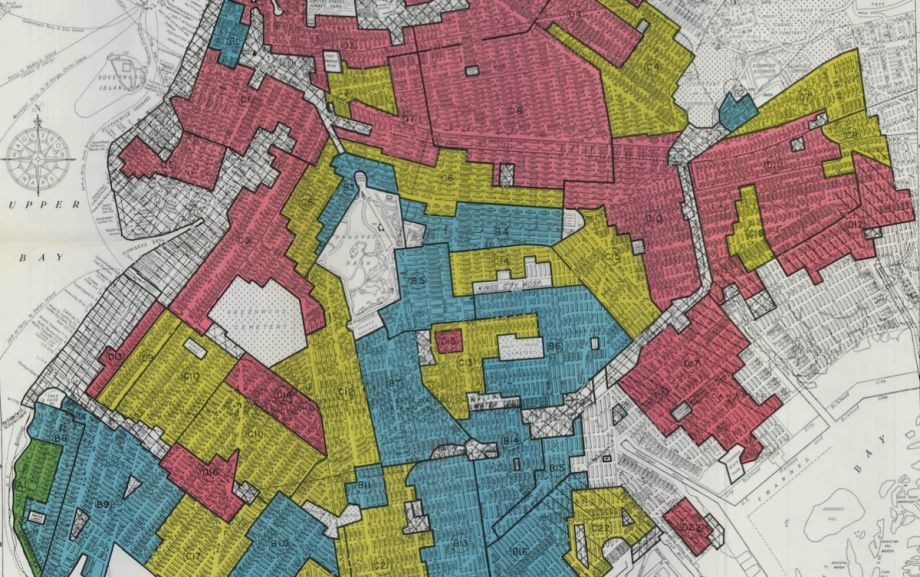

Their diverse district includes the neighborhoods of East New York, Cypress Hills and City Line. More than 182,000 people live here; half are black, and 36 percent Latino. Median income is around $32,000. The federal government redlined much of the neighborhood in 1938, shutting residents out of bank lending on the basis of race, despite banks holding deposits at branches located within the district.

Mullane and her neighbors met in community centers, church basements and parish halls, anywhere that anyone in the group had access to meeting space. They started meeting with bankers and banking regulators, going in armed with two things: One was the Community Reinvestment Act (CRA), passed in 1977, which created a regulatory framework to bring banks to the table to discuss credit needs with the communities in which they operate. It also officially outlawed redlining. The other thing Mullane’s group had was data.

“For the past seven years we have analyzed HMDA [Home Mortgage Disclosure Act] data for our census tracts, brought together the seven local lending institutions that serve Cypress Hills and City Line to discuss their performance and ways they should increase lending, and worked cooperatively with our banks to meet the credit needs of area residents and businesses,” Mullane testified. While she described many remaining shortcomings of bank lending in the neighborhood, she also testified that “the Reinvestment Committee has slowly turned around the redlining of our communities.”

Fast-forward to today. There are currently around $670 million in deposits at bank branches in Brooklyn Community District 5. The Cypress Hills/City Line Reinvestment Committee still meets monthly to discuss how to access a bigger slice of that pie. While the group remains vigilant against redlining and also the threat of gentrification, the newest push is for banks to provide more lending and other support for equitable economic development.

“We have to pick up the fight for living wage jobs, and really nurture the growth of sectors in our neighborhood that are gonna produce those living wage jobs, and work more intentionally with employers that have been shown to be good employers,” says Michelle Neugebauer, executive director of the Cypress Hills Local Development Corporation (CHLDC). Neugebauer testified at the same 1998 hearing alongside Mullane, and Mullane also served as president of CHLDC’s board of directors until she passed away in 2003.

The Reinvestment Committee and CHLDC are far from alone in the push for more equitable economic development in banks’ CRA obligations. CHLDC is a member of the Association for Neighborhood and Housing Development (ANHD). As part of their work, every year ANHD publishes a State of Bank Reinvestment report, analyzing the local impact of the CRA, highlighting industry trends, and identifying and comparing how individual banks do or don’t meet NYC’s credit and banking needs. The latest edition just came out, and increasing equitable economic development support continues to be a growing priority.

“We still need more affordable housing, and deeper affordability, but we have a really robust ecosystem for financing it,” says Jaime Weisberg, senior campaign analyst at ANHD. “We don’t have that around equitable economic development.”

Overall, according to the report, NYC bank reinvestment went up, and not just because banks are growing. Deposits at NYC’s 25 largest banks increased 14 percent, while reinvestment dollars from those banks went up 25 percent. That’s good news, Weisberg says.

When it comes to community development, things are mixed. The average community development loan size went up, but fewer loans went out in 2014 compared to 2013, so total community development lending was flat.

On equitable economic development, the picture is bleak. Eight of 20 banks reported that none of their community development loans fell under the economic development category. Only three banks reported that more than 1 percent of their CRA-qualified investments went for economic development. Meanwhile, the number of CRA-eligible small business loans increased by 10 percent, but total dollar amount loaned out declined by 9 percent. That could be a good thing, indicating that banks are being more responsive to small businesses needing smaller loans than in the past, but it’s hard to say.

“The numbers highlight the emphasis for quality over quantity, especially when you’re impacting low- and moderate-income people,” says Weisberg. “The numbers for economic development continue to be lower than they should be, but it’s a new area. We really think there’s an opportunity for more investment there, for both more dollars and for it to be quality investments.”

Working closely with local groups like CHLDC, Weisberg says, is the best way for banks to ensure they’re not just spinning the wheels, that they’re actually contributing to community economic development.

ANHD first introduced an equitable economic development section to their bank reinvestment report in last year’s edition, and this year they’re making an even stronger push. They’re calling for $1 billion in CRA equitable economic development activity, and also put forth a new proposal for an equitable economic development working group.

The proposed working group would include representatives from the NYC Economic Development Corporation, the Department of Small Business Services, the mayoral administration, financial institutions, community development, small business development, industrial development, workforce development and more. “We’ll be putting the pieces into place throughout the next year. We think it’s important that all the voices are present,” says Weisberg.

The working group would provide a focused environment to follow up and dive deeper into the equitable development discussions that pop up periodically between ANHD, local groups like CHLDC, regulators and banks. According to Neugebauer, local bank branch staff and CRA officers often attend monthly Reinvestment Committee meetings. Every year, sometimes with financial support from bank branches, the committee and CHLDC put on an annual banking forum, which also typically attracts bank staff. Just last week, Weisberg joined a tour of Queens neighborhoods with Congressman Gregory Meeks and U.S. Comptroller of the Currency Thomas J. Curry (his office is one of several agencies that performs regularly scheduled CRA examinations of banks).

More than any one recommendation, ANHD and its members hope an ongoing discussion about equitable economic development and the CRA will foster a financing ecosystem as robust as that for affordable housing.

Another important ongoing discussion, Weisberg says, is the one around revisions to the standard questionnaire regulators use in conducting regularly scheduled CRA examinations of banks.

“There’s the law, and there’s the regulation, and then there’s how they actualize the regulations, which is where the Q&A document comes in,” explains Weisberg. “This is a very, very important document that banks look to and regulators look to, for how they implement the CRA.”

The last round of revisions came out in 2010. Clarifying guidance on economic development is a priority in the current back-and-forth among banks, regulators and advocacy groups like ANHD, the California Reinvestment Coalition, and the National Community Reinvestment Coalition. Weisberg isn’t sure when the final Q&A will come out, but, “It’s a really exciting time in CRA advocacy,” she adds.

In the meanwhile, despite the CRA’s shortcomings (like the fact that 98 percent of banks receive satisfactory or outstanding CRA ratings), at least some banks are already experiencing regulator interest in equitable economic development. Some have even been proactive about it.

“In the past there was a lot of focus on affordable housing, and there still is, but especially if you have branches or stores like we do, regulators want to see that you’re active in the communities,” says Peter Meyer, market president for NYC at TD Bank, which has been active in providing grants to local chambers of commerce, as well as lending capital to nonprofit, mission-based small business lenders like ACCION.

Meyer adds, “If you’re active in the community, then [regulators want to see] where are you putting your money, are you putting your money to small businesses in low- to moderate-income areas, is it helping economic growth and activity. The focus is changing.”

The Equity Factor is made possible with the support of the Surdna Foundation.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)