Are You A Vanguard? Applications Now Open

Single-family homes on Loughborough Avenue in Carondelet, a stable middle neighborhood in southeastern St. Louis.

Photo by prettywar-stl via Flickr

This is your first of three free stories this month. Become a free or sustaining member to read unlimited articles, webinars and ebooks.

Become A MemberEditor’s note: The following is an excerpt from the policy brief and working paper America’s Middle Neighborhoods: Setting the Stage for Revival (Lincoln Institute of Land Policy, 2018). Next City was pleased to welcome Alan as the featured speaker in our November 19 online seminar series. Donate here to support Next City’s journalism and events. If you become a Next City sustaining member at $5 per month, or if you donate $50 or more, you will receive Mallach’s “The Divided City” as a thank-you gift.

The dramatic rise of American industry in the nineteenth and twentieth centuries drew millions of workers into U.S. cities, triggering the expansion of the nation’s urban middle and industrial working classes. Across the country, “middle neighborhoods” sprang up to house these middle-income households: blocks of single-family homes connected by busy arterial streets, with businesses, houses of worship, public schools, and distinct ethnic or racial identities that sustained a social fabric paralleling their physical form.

Despite ongoing challenges, many of these neighborhoods survive today. Containing 25 to 40 percent of the population of most older cities, they remain a major part of the urban life and economic viability of their cities, especially in postindustrial hubs known as “legacy cities.” In an era of increasing polarization and inequality, these still-diverse middle neighborhoods also offer opportunities to striving working-class, minority, and immigrant families. They also contain valuable urban assets: homes, infrastructure, utility systems, parks, schools, community centers, and commercial and industrial buildings.

In recent decades, however, the trajectories of America’s middle neighborhoods have diverged. Many in “magnet” cities such as Seattle or Washington, D.C., have seen impressive revival or gentrification, but, in legacy cities such as Baltimore or Cleveland, middle neighborhoods often face decline. The resulting losses — of jobs, people, real-estate value, and more — threaten these cities’ futures, and addressing decline before it becomes irreversible is no easy task.

These middle neighborhoods are at risk — not from a single factor, but a series of separate changes that amount to something close to a perfect storm. Although the in-migration of millennials and immigrants driving urban revival in many legacy cities has helped some middle neighborhoods counter negative pressures, these groups are settling in a relatively small number of neighborhoods. Many more neighborhoods continue to be buffeted by the stress of demographic and economic change, aging housing stock, suburban competition and more, often exacerbated by adverse public policies. And nowhere are these risks greater than among the many middle neighborhoods in our cities that for decades have housed much of the nation’s African-American middle class.

Often overlooked, middle neighborhoods matter — both to the people who live in them and to their cities and regions — and solutions demand engagement not only from the neighborhood itself but also from the city, region, and state. Nothing less than the fate of millions of people and dozens of cities lies in the balance.

Middle neighborhoods are further undermined by powerful economic trends at the national level:

Greater income inequality has thinned out the middle class, leaving fewer such households to fill these neighborhoods;

“Income sorting,” or increased residential segregation by income level, multiplies the effects of inequality; and

The changing character of the economy and workforce has eroded jobs and opportunities for workers in legacy cities.

Furthermore, as powerful changes ripple through American society — including declining fertility rates, changes in immigration policy, technological shifts, and climate change — the effects on middle neighborhoods will be impossible to predict.

Although middle neighborhoods typically share a predominately single-family housing inventory, the characteristics of that housing stock vary greatly from one neighborhood to another. Houses vary by size, architectural character, materials, and other features. That stock, however, shares one feature: it is old. Moreover, being largely single-family, regardless of age, it is not always a good fit with today’s housing market demands.

Legacy city middle neighborhoods were largely built from the late 19th century through the 1960s. Since the 1960s, little new housing has been built in these areas except for subsidized housing. 90 percent of the single-family homes in Cleveland and in Pittsburgh predate 1960; even in most inner-ring ‘starter home’ suburbs, 75 percent to 90 percent of the single-family homes were built before 1960. Although a handful of older homes have been rehabbed, largely with public funds, they make up a minute share of the total housing stock.

These middle neighborhoods were designed for married couples raising children, which in 1960 included up to 45 percent of all households living in legacy cities. As of 2016, however, the number of such households had declined nationally to 19 percent — and far more in some cities, falling to 9 percent in Pittsburgh and just 7 percent in Cleveland. A comparable alternative source of demand for these neighborhoods has yet to emerge.

Shaw is an example of a stable St. Louis middle neighborhood, having benefited from a proximity to downtown and a housing stock that features distinctive architecture. (Photo by Paul Sableman via Flickr)

Today, much of the demand for urban housing today comes from single individuals, couples, and people in informal living arrangements. Much of the housing in middle neighborhoods may not appeal to them. While those few neighborhoods with distinctive architectural or historical character and which are close to downtown or major institutions, such as Shaw in St Louis, Hampden in Baltimore or Allentown in Buffalo, may draw them, most middle neighborhoods lack either or both features.

Observers suggest that most older houses in these neighborhoods have not been upgraded or modernized to any significant degree, while many suffer from significant deferred maintenance and repair needs. The fact that many modest older houses have only one bathroom can itself be a significant deterrent to prospective homebuyers. NeighborWorks Rochester has created the Half-Bath Program, adding half bathrooms to houses in the Triangle neighborhood to build a stronger homebuyer market in the area.

This situation has severe consequences for middle neighborhoods by undermining potential housing demand. Even in areas where homebuyers may want to live, the condition of the houses on the market may deter many. Without a major infusion of public or private capital in the coming years, much of the housing in middle neighborhoods is at risk of deteriorating further, potentially to the point of no return. The increase in vacancies in many middle neighborhoods suggests that this is already happening. The question arises whether the capital is available and whether the demand exists to either to upgrade these houses or replace them with new houses or apartments that better reflect market preferences.

Assembling the capital to either repair and upgrade, or replace, a significant part of the existing housing in middle neighborhoods may be extremely difficult. Public funds are likely to fall far short of what is needed, and are largely restricted to means-tested households, in the case of Low-Income Housing Tax Credit (LIHTC) developments, to those earning 60 percent or less of the HUD-defined area median income. Building new subsidized housing to replace older market housing is unlikely to stabilize middle neighborhoods and may, under certain conditions, further destabilize them. The fate of these neighborhoods is likely to depend ultimately on their ability to attract private capital, whether through individuals buying and improving homes or private market contractors or developers rehabilitating existing houses or building new homes or multifamily buildings for the marketplace.

Attracting private capital will depend on drawing not only demand, but demand at income levels capable of moving neighborhood house prices to levels where they support substantial investment in existing houses and construction of new housing without public capital subsidy. Given the demographic and economic forces working against middle-market neighborhoods described earlier, the generally low market values in legacy cities, continuing gaps in mortgage access, and ongoing competition from nearby inner-ring suburban markets, this will be a daunting challenge for those areas that lack the special attributes likely to render them particularly desirable.

High levels of homeownership have historically been typical of middle neighborhoods in legacy cities as well as elsewhere in the United States. Homeownership rates in the United States, after peaking at 69 percent in 2004, dropped to 63 percent by 2016, from which low point they have since begun to rebound. Both homeownership rates and the number of homeowners have dropped sharply in legacy cities since 2000.

There may be many reasons for the erosion of homeownership in middle neighborhoods, beginning with the decline in middle-income demand reflecting the demographic shifts described earlier. That is far from the only factor. Many middle neighborhoods were victimized by subprime lending and foreclosures, a process that as homeowners lost their homes, and lenders subsequently resold them, led to widespread shifts from owner-occupancy to absentee ownership. More recently, impediments to home-buying in the form of the increase in student debt and in the reluctance of lenders to make mortgages for low-value properties, particularly to homebuyers with less than pristine credit, have been recognized, although not addressed.

Since the end of the Great Recession, it has become harder for moderate and middle-income families, particularly those with less-than-stellar credit scores, to get mortgages. While nearly 2 out of 5 American households have credit scores under 660, they accounted for fewer than 10 percent of the mortgages made between 2011 and 2015. This problem is exacerbated by the fact that house prices in many struggling middle neighborhoods are extremely low, under and often well under $50,000. As a 2015 Urban Institute report pointed out, “Getting a mortgage loan for less than $50,000 has never been easy, but it’s becoming next to impossible.”

Although some commentators have argued that a shift from homeownership toward rental tenure is not a problem, and perhaps even salutary, we believe that the loss of homeownership in middle neighborhoods may have many negative consequences. The residential stability as well as community engagement more typical of homeowners than of renters, both of which are critical elements in the vitality of middle neighborhoods, are likely to erode, particularly in light of the extreme economic insecurity of the lower income renters likely to replace homeowners in struggling middle neighborhoods. Moreover, particularly in neighborhoods where house sales prices are severely depressed relative to rent levels, absentee landlords are not only unlikely to make the capital investment necessary to maintain aging housing stocks, but may actively “milk” their properties, disinvesting in them to focus entirely on short-term cash flow.

The decline in homeownership in middle neighborhoods is widely coupled with a decline in sales prices, particularly in communities which experienced a housing bubble during the years prior to 2006. The combination of loss of owners and lower house values has led to a massive loss of wealth on the part of middle-income homeowners, particularly in African-American neighborhoods. A recent study of St Louis middle neighborhoods found that in just one census tract homeowners experienced a loss of over $35 million in home equity between 2008 and 2016.

Predominately African-American neighborhoods on St. Louis' Northside, such as O’Fallon, pictured here, boast handsome houses on tree-lined streets. But their lack of proximity to downtown, with its major universities and medical centers, has made these areas a less attractive housing option, and the neighborhoods have suffered for that disinvestment. (Photo by Michael Allen via Flickr)

Locational assets drive neighborhood change. In fact, the single most important factor in upward market change for a struggling area is proximity — to strong neighborhoods, downtowns, major institutions, or well-maintained parks and bodies of water. Because most middle neighborhoods were built with amenities such as schools, houses of worship, and retail stores within walking distance, these areas are often at a locational disadvantage in today’s cities. Once-high homeownership rates in these neighborhoods have eroded, reflecting demographic shifts as well as the devastating effects of subprime lending and the foreclosure crisis, which hit these neighborhoods disproportionately hard. As housing continues to age, weak demand and low property values make rebuilding and repopulating these neighborhoods increasingly difficult. Even as demand has reemerged, lower sales prices and severe constraints on mortgage access have led to a massive loss of wealth by middle-income families, particularly in the African-American neighborhoods that were hit hardest.

After the “white flight” of the 1960s and 1970s, many urban middle neighborhoods were repopulated by middle-income African-Americans, and these remained viable communities for decades. Since 2000, however, these neighborhoods have lost disproportionate ground, devastated by the 2008 foreclosure crisis and by rapidly increasing suburban out-migration. Many such neighborhoods have seen homeownership erode and property values collapse. Thousands of homeowners lost most of their wealth, while many fled cities for nearby suburbs. In cities such as Detroit, hundreds of once-vital neighborhoods are in deep decline, with devastating impacts on their residents’ quality of life, the wealth of African-American families, and the social health of their cities.

The trajectories of middle neighborhoods in St. Louis illustrate the range of challenges and opportunities. In recent decades, the number of middle neighborhoods in the city has shrunk; some have revived, some declined, and a few remained stable. These trends, however, have proven uneven. Many racially and ethnically mixed Southside neighborhoods such as Shaw or Fox Park, once struggling, have rebounded with rising property values and an inflow of young home buyers. But middle neighborhoods in the predominately African-American Northside, like O’Fallon or Penrose, have declined. Despite their handsome houses on tree-lined streets, they also lack the proximity that Southside neighborhoods have to the Central Corridor, where the city’s major universities, medical centers, and downtown are located. Unless concerted, immediate action is taken, St. Louis could lose many of its finest neighborhoods — and much of its African-American middle class.

Two additional factors have led to black middle neighborhoods being disproportionately affected by shrinking demand. First, despite some change over recent years, market demand is still strongly racially segmented. While black buyers are willing to buy homes in neighborhoods of all racial configurations, and some white buyers are increasingly willing to buy in racially mixed areas, they continue to avoid areas that are predominately African-American, particularly in those parts of cities that have been defined as distinct racial “territories”. The same appears to be true of suburban areas where black populations are increasing, as well of the likelihood of any individual urban neighborhood seeing market revival in the form of gentrification. Thus, little of the large white demand pool reaches predominately black areas, while the smaller black demand pool is dispersed across all of the region’s neighborhoods.

Leaving aside the powerful implications of that dynamic from the standpoint of social equity, segregation and wealth, it has a distinct market effect: it means that the pool of potential buyers for houses in African-American middle neighborhoods is far smaller than in mixed or predominately white neighborhoods, creating what could be called a ‘segregation tax” that reduces potential demand and depresses sales prices and wealth accumulation. It also means that while market forces may lead to stabilization and upward economic movement in many — although not necessarily all — predominately white middle neighborhoods, they are far less likely to have similar effects in physically or economically similar predominately black neighborhoods.

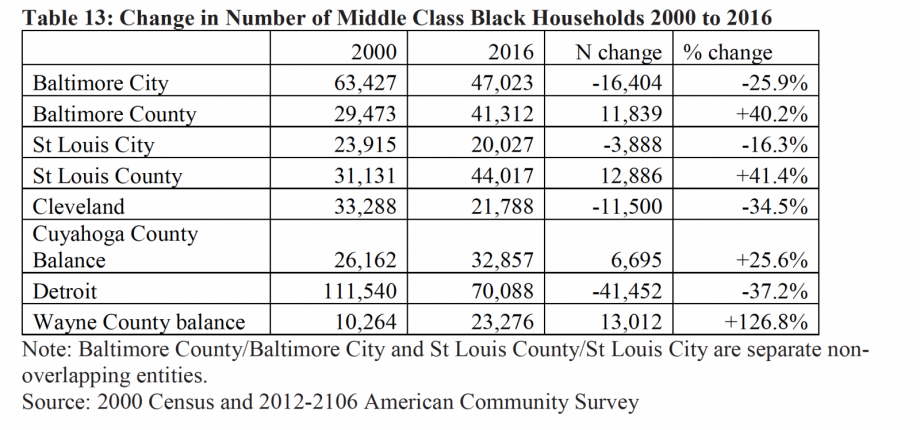

The second issue piggybacks on the first. For many reasons, the rate of out-migration of middle-income households from urban areas has increased significantly since 2000, a pattern of “black flight” that in some respects parallels the “white flight” of the 1960s and 1970s. The effect of this trend can be seen in the shift in the distribution of middle-class African-American households (defined here as households earning $35,000 to $100,000 in constant 2016 dollars) from the central city to their nearest suburban neighbors since 2000, as shown in the table below.

Out-migration from black middle neighborhoods simultaneously increases housing vacancies while reducing the demand for housing in those neighborhoods. Many of the properties vacated by homeowners are bought by absentee investors or abandoned by their owners, both outcomes potentially hastening the neighborhood’s decline.

From a market perspective, these neighborhoods are at a competitive disadvantage to primarily suburban neighborhoods. While some families moving from black middle neighborhoods may move to other, racially mixed, parts of the same city, the numbers suggest that the great majority moved to the suburbs, or (since in three of the four areas shown suburban growth was much less than urban decline) outside the metropolitan area entirely.

In contrast to high-cost regions such as New York or Seattle, where homes in even relatively modest suburbs tend to be out of reach of most working-class families, inner suburbs around cities such as Detroit, Cleveland, or Cincinnati tend to be reasonably priced, and often accessible to families with incomes as low as $30,000. Many of these suburbs, moreover, appear to offer advantages over central-city neighborhoods, particularly for families with children. Suburban relocation appears to confer significant marginal benefits with respect to both education and crime, at modest incremental cost. For the two-thirds or more of the urban workforce in many cities who already work in the suburbs, the appeal of moving to the suburbs is clear. We stress “appear to,” since those advantages are not always present in reality. While many city residents undoubtedly benefit from moving to the suburbs, many citizens, such as those who moved to Ferguson and other North St Louis County suburbs in the 1990s and 2000s, have found themselves arguably worse off than before.

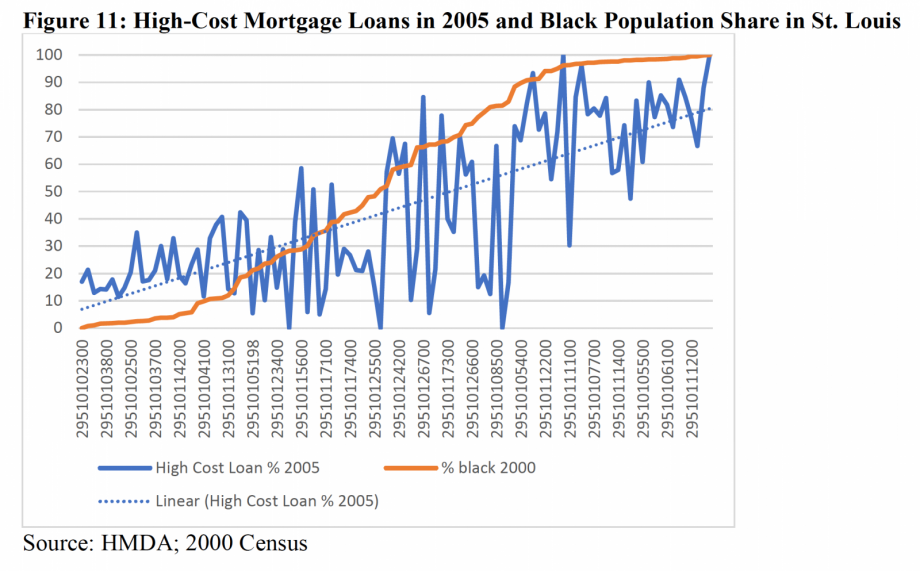

These cities are losing a critical battle for the people who more than any other have sustained their middle neighborhoods for many decades — the African-American working- and middle-class family. The decline in demand has taken place at a time when black middle neighborhoods were also being hit hard by the foreclosure crisis that followed the subprime lending frenzy of the early years of the millennium. The figure below illustrates the relationship between subprime lending in 2005 and black population share in St Louis; in that year, 74 percent of all mortgage loans made in neighborhoods that were 90 percent or more black were high-cost loans, compared to 20 percent of mortgage loans in areas that were less than 10 percent black.

As a result, black neighborhoods were hit particularly hard by the wave of foreclosures triggered by subprime mortgages as the housing bubble burst. These foreclosures have not only had a severe impact on the lives and wealth of the families losing their homes to foreclosure, including moves to rental housing and often to less-desirable neighborhoods, but also destabilized entire neighborhoods.

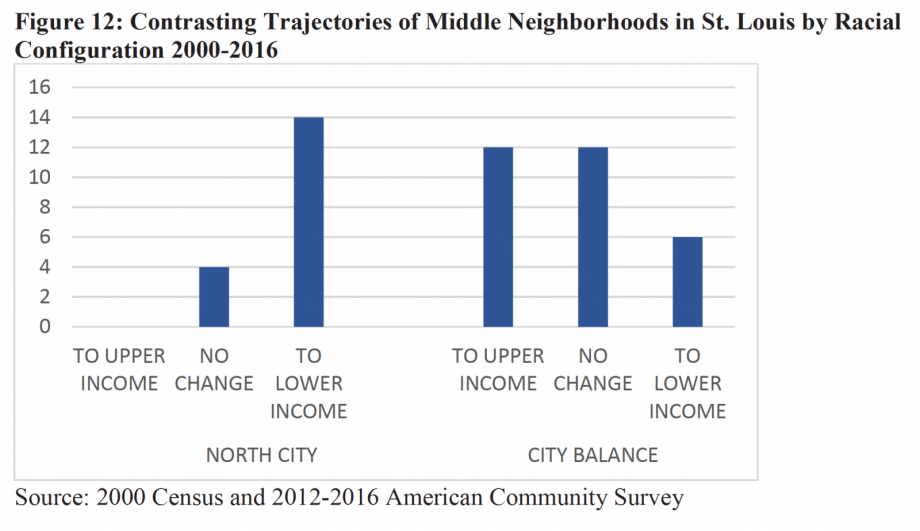

The impact of these factors is visible in St Louis. That city is divided between North City, an almost entirely African-American area north of the Central Corridor, the Corridor and South City, a checkerboard of predominately white and racially mixed areas. The trajectories of those areas that were middle neighborhoods (based on median income) in North City in 2000 from 2000 to 2015 were markedly different from those of the middle neighborhoods in the balance of the city, as shows in the figure below.

Nearly 80 percent of the middle neighborhoods in North City moved downward and became lower-income neighborhoods by 2015, while none moved upward. In South City, 40 percent moved upward, 40 percent remained middle neighborhoods, and only 20 percent moved downward. The ability to rebuild homebuyer demand in these neighborhoods is further limited by the constraints on mortgage lending that have emerged since the end of the foreclosure crisis, as described above.

Middle neighborhoods face powerful forces of change that threaten their vitality and have already pushed many into decline. While some of these factors (such as national demographic shifts) may be beyond the influence or control of local stakeholders, other factors (such as public policy) call for creative local initiatives. These strategies for the revival of middle neighborhoods can become the framework for specific recommendations for policymakers and practitioners

Prioritize Middle Neighborhoods in Local Planning and Revitalization Strategies. American local governments have often neglected middle neighborhoods, but they are critical to the future health and stability of legacy cities. Addressing them does not mean neglecting seriously disinvested low-income areas, nor does it create a back door to gentrification. Preserving these valuable physical and social assets benefits the entire city.

Increase Access to Capital. When home buyers and owners have difficulty getting mortgages or funds for property upgrades, it further impedes the stability and revival of struggling middle neighborhoods — particularly those with already-low property values. Local and state governments should actively work with lenders and regulators to improve access to capital for middle neighborhoods.

Design Context- and Market- Sensitive Strategies. One size does not fit all. Middle neighborhoods vary widely by location, physical form, demographics, migration and citywide and regional conditions. Strategies and interventions that may be highly effective in one neighborhood or set of conditions may be much less effective in others. Neighborhood-based strategies — in middle neighborhoods and elsewhere — must be grounded in solid data on each neighborhood’s social capital, collective efficacy, and market trends.

Support Bottom-Up Community Efforts. Neighborhoods are social as well as physical entities, and robust social capital can promote stability and stave off decline. Local and state governments should support neighborhood-driven efforts to build and sustain strong communities in conjunction with programs to improve physical conditions and foster homeownership.

Target Research Efforts to Build Greater Understanding. Middle neighborhoods still raise more questions than answers: Why do some thrive while others decline? Which strategies work under what conditions to stabilize or revive them, and why? A systematic research effort should answer these questions and more in ways that add value to the work of practitioners and policymakers.

Excerpted from America’s Middle Neighborhoods: Setting the Stage for Revival, by Alan Mallach. Copyright © 2018 by Lincoln Institute of Land Policy. Reproduced with permission of Lincoln Institute of Land Policy, Cambridge, Massachusetts.

Alan Mallach is a senior fellow at the Center for Community Progress and a visiting professor at the Pratt Institute Graduate Center for Planning and the Environment. He is the coauthor of the 2013 Policy Focus Report, Regenerating America’s Legacy Cities, and editor of the 2012 book Rebuilding America’s Legacy Cities: New Directions for the Industrial Heartland. His newest book, The Divided City: Poverty and Prosperity in Urban America, released in June 2018.

Next City is a nonprofit news organization that believes journalists have the power to amplify solutions and spread workable ideas from one city to the next city. Our mission is to inspire greater economic, environmental, and social justice in cities.

Learn more about us →

20th Anniversary Solutions of the Year magazine