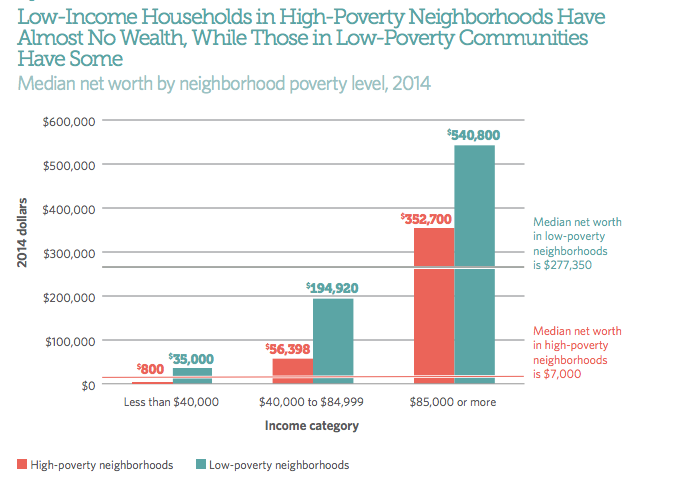

The typical low-income household in a high-poverty neighborhood has only $800 in accumulated wealth. A household with a similar income in a wealthier neighborhood has $35,000 in accumulated wealth — more than 40 times that amount. The latter’s also more likely to be a homeowner and have checking and education savings accounts, according to new Pew data released last week.

The report illustrates that not only does neighborhood poverty correlate with unemployment, lower-performing schools and increased violence, but it also affects financial security, regardless of income. Here, more of the findings.

The difference between high- and low-poverty neighborhoods is stark. Middle- and high-income households in high-poverty communities have nearly $200,000 less accumulated wealth on average than similar households in low-poverty neighborhoods. Overall, the residents of low-poverty neighborhoods are almost twice as likely to own their own homes — and their homes are worth nearly three times as much — when compared to residents of high-poverty neighborhoods.

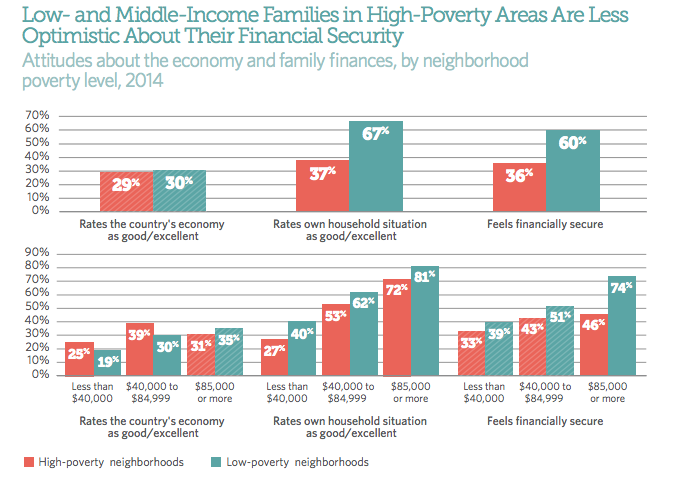

Regardless of income, households in communities with concentrated poverty experience higher levels of both actual and perceived financial instability. The difference is largest among the wealthy: Only 46 percent of households making $85,000 or more in high-poverty neighborhoods feel financially secure, compared to 74 percent in the same income bracket in wealthier neighborhoods.

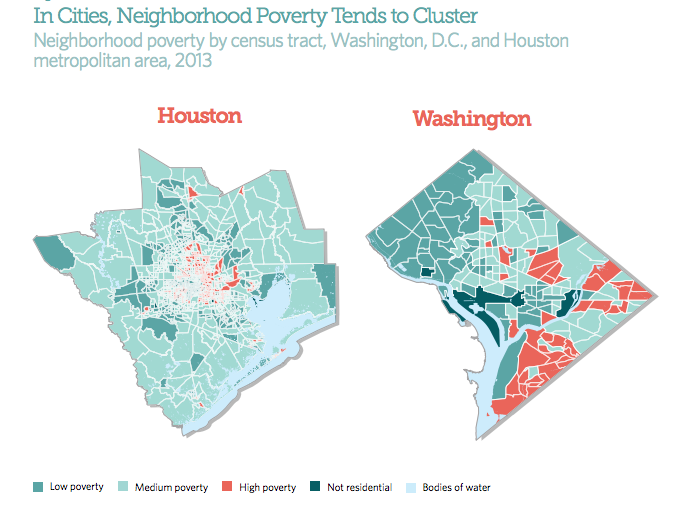

Neighborhood poverty is characterized by the percentage of houses living in poverty within a particular census tract. Both high- and low-poverty areas tend to cluster geographically, and the problem of concentrated poverty is only deepening in American cities. Nearly 40 percent of the urban poor live in high-poverty areas today, compared to 28 percent in 1970. Between 2000 and 2011, concentrated poverty increased by 50 percent.

The situation is especially dire for black households. In nine states, one in nine black people lives in a high-poverty area.

According to the Pew report, “As the concentration of poverty decreases across neighborhoods, so does racial diversity. Three-quarters of the residents of low-poverty neighborhoods are white, compared with just one-third in high-poverty communities.”

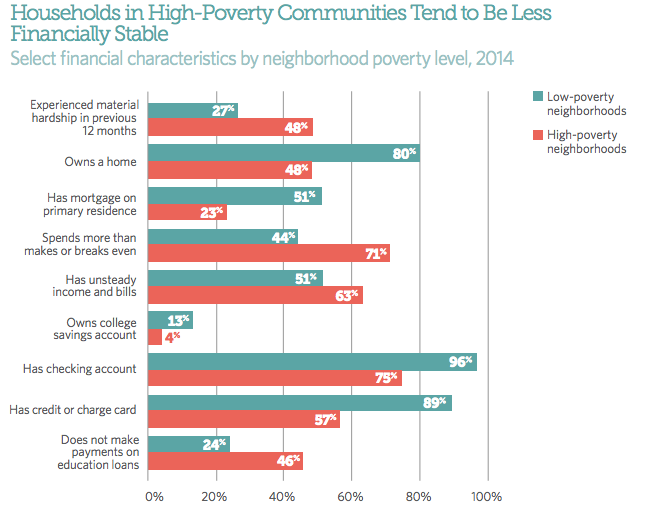

Neighborhoods with higher concentrations of poverty also have higher percentages of households headed by single people, and lower percentages of college graduates — though high- and low-poverty communities have similar percentages of residents with some college education.

Jen Kinney is a freelance writer and documentary photographer. Her work has also appeared in Philadelphia Magazine, High Country News online, and the Anchorage Press. She is currently a student of radio production at the Salt Institute of Documentary Studies. See her work at jakinney.com.

Follow Jen .(JavaScript must be enabled to view this email address)