After receiving final approval from regulators on March 18, Arise Community Credit Union — Minnesota’s first Black-led credit union — is out to set an example as a credit union founded in direct response to systemic violence manifested in the form of bodily violence. As my colleague Deonna Anderson reported for Next City nearly six years ago:

One week after Philando Castile was murdered by a police officer in a Twin Cities suburb in 2016, community members gathered on the historically black north side of Minneapolis. Over 200 residents showed up to a meeting organized by Blexit, a grassroots organization addressing inequity in Minnesota and the wider U.S.

The residents took part in small and large group discussions. They talked about what they wanted to invest in and divest from. They wrote their ideas in marker on butcher paper posted on walls throughout the meeting space. Then they voted on their most pressing priorities.

The number one idea, which garnered twice the amount of votes than any other idea on the board that night, was to establish a Black-led credit union on the northside of Minneapolis.

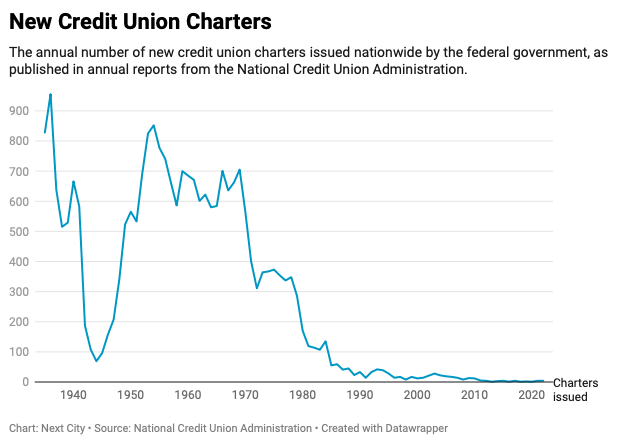

Chartering a new credit union today is like traversing a long lost trail through the woods, one that used to be well-traveled but is now overgrown, littered with fallen trees and other obstacles no one has had to navigate in many years. Prior to 1970, there were 500 to 600 new credit unions chartered across the country every year. After a steep decline to near zero, the numbers have never recovered. Over the past 10 years, fewer than 30 new credit unions have been chartered across the country.

According to Inclusiv, a network of credit unions that focus on community development, minority credit unions across the country are closing at the rate of one per week, making the new Arise Community Credit Union’s chartering even more urgent if that trend is to ever be reversed. Organizers began raising deposits by going door-to-door, canvassing at bus stops and other places where neighbors on the north side gathered. They eventually amassed over 1,100 deposit pledges totaling more than $3 million — and that became part of their pitch for support from the City of Minneapolis.

“We were simply saying, ‘Guess what, 1,100 black community members on the north side decided they were going to do this and they’ve already put down $3 million and we’re asking you to come behind them and to acknowledge and affirm the commitment they’ve made,” Me’Lea Connelly, who was leading the effort at the time as executive director of the Association for Black Economic Power, told us in 2019. “It wasn’t coming in with our hands out, we came in with a full deck.”

Arise hopes to fill in the gap left behind by other more conventional banks and even other credit unions. Predatory lenders have jumped into the gap left behind by the retreat of the mainstream banking system from certain communities. African Americans are twice as likely to live within 2.5 miles of a payday lending storefront, compared with all Minnesotans.

After years of advocacy, last year Minnesota Governor Tim Walz signed a bill establishing an interest rate cap on loans in the state. While advocates had been calling for a 36% rate cap, the final bill as signed into law sets an overall cap of 50% while instituting a new requirement for lenders to evaluate a borrower’s ability to repay for loans between 36-50%.

Currently, 18 states plus the District of Columbia have established lending rate caps of 36% or below, according to the Center for Responsible Lending. The caps have proven their effectiveness. Nebraska voters passed a 2020 ballot measure to establish a 36% rate cap in their state, and since then payday lenders have disappeared across Nebraska, the Omaha World-Herald reported in May 2023.

In Arkansas, instituting a lending rate cap led to the last payday loan storefront in that state closing in 2009. Since then, Arkansas retail borrowers say they’re better off, and they’ve been finding their way to safer, non-predatory options — including new options like People Trust Community Federal Credit Union, a Black-led credit union chartered last year and that state’s first new credit union since 1996.

In 2021, 39 licensed payday lending entities in Minnesota made 176,241 payday loans to 20,004 Minnesotans, according to the Minnesota Department of Commerce. The average borrower took out nine payday loans, at an average loan amount of $365, and was charged an average of 197% interest per loan. There’s a growing pile of evidence that payday lenders tend to place their storefronts in Black neighborhoods like those on the Northside of Minneapolis.

As those lenders retreat, Arise can be there to start picking up the pieces.

Chartering a new credit union is a huge lift. It’s been nearly eight years of organizing for Arise, but it’s not uncommon for aspiring credit union organizers to take multiple years between initial conversations to raising startup capital to finally getting a new charter. The Association for Black Economic Power also had to deal with a leadership transition along the way — it’s now led by Debra Hurston. The new credit union has its own CEO, Daniel Johnson, who has deep family ties and professional ties to the Northside of Minneapolis.

It would have been easier — and quicker — for Hurston if her group just brought in an existing bank or credit union as a partner organization to provide access to credit and basic financial services to the Northside.

But Hurston says in surveys, town halls and just informal conversations over the years, the Northside’s desire for its own institution has only gotten stronger.

“The mistrust in the banking community, it’s not a small thing, and it can’t be fixed overnight,” Hurston told me last year. “We’re starting from the wrong spot…if I have to protest in front of you to make you treat me right. Something’s not right about that. So no one from our communities has ever asked me if we should just partner with a larger bank.”

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)

Add to the Discussion

Next City sustaining members can comment on our stories. Keep the discussion going! Join our community of engaged members by donating today.

Already a sustaining member? Login here.