Are You A Vanguard? Applications Now Open

In October 2017, Fresno-based Central Valley Community Foundation announced a $2.6-million deposit into Self-Help Federal Credit Union’s Fresno branch, making this community foundation the branch’s largest single depositor.

Credit: Self-Help Federal Credit Union

This is your first of three free stories this month. Become a free or sustaining member to read unlimited articles, webinars and ebooks.

Become A Member

On an average day at Self-Help Federal Credit Union’s branch in Fresno, Calif., ten or so people come in to sign up as new members, and around 20 people submit applications for home mortgages, car loans, small business loans or personal emergency loans (for as little as $500). Since opening in August 2015, this one branch has made more than 1,000 loans and counting. But these aren’t just any borrowers. At this branch, 70 percent of borrowers come from low-income households, and 91 percent are people of color.

Branch Manager Rosa Pereirra has witnessed those borrowers reclaim power over their financial lives in ways that still surprise her, even after 28 years in banking.

“Some of the folks coming in making $12.50 an hour, they’ve got $15,000 in their savings account,” says Pereirra. “I make a good living, but I don’t have $15,000 in my savings account.”

These borrowers and this branch are the exceptions and not, unfortunately, the rule. In the state of California alone, payday lenders make billions of dollars in payday loans per year, earning hundreds of millions in interest and fees — all largely targeted at low-income households and communities of color.

California-licensed payday lenders earned $458.5 million in fees on payday loans in 2016, according to the latest annual report from the state’s Department of Business Oversight. Nearly 75 percent of those earnings, $343 million, came from customers who took out seven or more payday loans. Some 77 percent of payday loan borrowers in California earn less than $40,000 a year — and payday lenders are more likely to set up shop in predominantly black or Latino neighborhoods, according to a separate study from the same department.

Self-Help’s Fresno branch, in the overwhelmingly Latino southeast part of the city, was the Federal Credit Union’s first “de novo” (the banking term for new) branch in the state. (Self-Help, based in North Carolina, had earlier merged with several other struggling credit unions in California.) Pereirra leaped at the chance to take on a leadership role at Self-Help, a financial institution created in 1980 to serve the underserved. She had 28 years of experience in community banking and credit unions in Fresno, as well as ten years of experience serving on the board of directors of a local food bank.

“Not to put other banks down,” she says, “But for the first time in my career, I really feel like I’m helping people.”

Pereirra realizes that other banks are still an important part of her work today, at a credit union branch that’s not yet three years old. As nonprofit organizations, credit unions can’t raise capital from traditional investors, so one of the biggest early sources of cash for a new credit union branch are other, larger banks and credit unions. Central Valley Community Bank, Fresno First Bank, and Educational Employees Credit Union (where Pereirra used to work) all have deposits at Pereirra’s branch. “They understand we’re not in competition for the same people,” says Pereirra.

Those big early deposits provide a source of cash to begin making loans, a necessary step for the branch to generate income. It’s especially important to get deposits from outside of your core market when your core market consists of underserved, low-income households and entrepreneurs who don’t have large deposits to start with.

Self-Help Federal Credit Union Branch Manager Rosa Pereirra. (Credit: Self-Help Federal Credit Union)

So imagine Pereirra’s excitement last October, when, after a few months of conversations and standard financial due diligence, the Fresno-based Central Valley Community Foundation announced it was depositing $2.6 million into Self-Help Federal Credit Union’s Fresno branch, instantly making the community foundation the branch’s largest single depositor and growing the branch’s deposit base from $9.7 million to $12.3 million. Pereirra describes the $2.6 million as the equivalent to 20 home mortgages or 175 car loans. Since October, her branch has already made another $2.6 million in loans across its portfolio, she says.

Central Valley Community Foundation’s deposit is just one example of a growing trend, where community foundations venture beyond grantmaking to realize the difference they can make by moving the cash in their coffers out of Wall Street and into investments that support the same communities that give these foundations their names — and their dollars.

“This deposit, it’s not just going to help people now, it’s going to help people for years to come,” says Pereirra. “In families that I’ve touched, you have generations of non-homeownership, then all of a sudden you have one person buy a house, and it seems that the rest of the family starts to buy a home. It happens a lot in our low-income families. Once they buy a house, it makes a ripple effect with the rest of the family members.”

As of 2017, community foundations across the United States held more than $91 billion in assets, according to the latest available data from the Foundation Center, which surveys and monitors public, private and community foundations. That same year, community foundations took in another $9.7 billion, and gave out $8.3 billion in grants. It’s not uncommon for community foundation assets to grow every year.

Community foundations bring in money from a variety of different sources. Some of it comes from galas, celebrity golf outings or other fundraising events. Some comes from corporate giving programs, when companies match employee donations. Some gets bequeathed in a person’s last will and testament. And about a quarter of community foundation assets comes in the form of donor-advised funds.

Donor-advised funds are a financial instrument for people who want to take advantage of the charitable deduction on their federal income taxes, but don’t necessarily have the time to pick a specific charity to receive those funds. If you put the money you earmarked for donation in a DAF, you can take the charitable deduction on your federal income taxes for that year. Then at a later date, you can direct that donation to the charity or charities of your choice. Some people just give instructions to their donor-advised fund manager, such as “give my money away to arts and music education” or “give out grants to help beautify parks.” Some just let the fund manager decide what to do with it.

Donor-advised funds have become increasingly popular by themselves, and community foundations aren’t the only ones offering donor-advised funds as a service to those who can afford them. In 2016, the Chronicle of Philanthropy reported that Fidelity Charitable Gift Fund, a donor-advised fund managed by Fidelity Investments, knocked off United Way as the largest annual recipient of philanthropic donations.

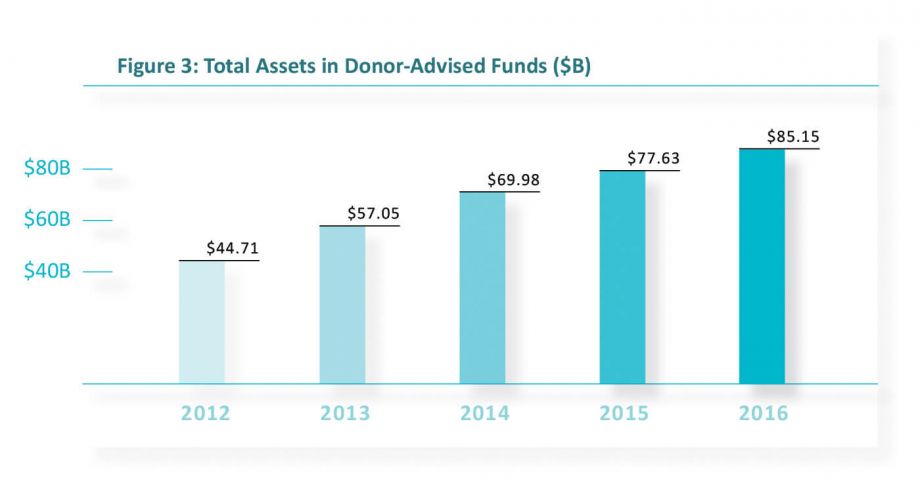

As of 2016, donor-advised funds held $85.15 billion in assets, growing ten percent from the year before, according to the National Philanthropic Trust’s annual donor-advised fund market report. There were 284,965 donor-advised funds as of that year, up 6.9 percent from the year before. Also in 2016, $23.27 billion went into donor-advised funds, and $15.75 billion was granted out from donor-advised funds.

But where do the dollars go in between being gifted to a community foundation and being granted out later? The short answer is Wall Street, to big investment houses whose responsibility is to maximize the financial return on those assets, even though the owners of those assets can’t take them back without paying a penalty and taxes on those funds. In maximizing the financial return, donor-advised fund clients should later have more funds to give away. As Fidelity Charitable’s website reads: “Your donation is also invested based on your preferences, so it has the potential to grow, tax-free, while you’re deciding which charities to support.”

Some community foundation money does end up in community banks — in addition to the deposit it made into Self-Help Federal Credit Union, Central Valley Community Foundation also maintains its operating account at Central Valley Community Bank. But as with other community foundations, the bulk of Central Valley Community Foundation’s assets are managed by more traditional investment houses that invest those funds in stocks, bonds and other assets around the world.

All across the country, however, there’s been an uptick in the number of community foundations that are moving money out of big investment houses and into more local investment options.

As Next City reported previously, the Chicago Community Trust created the “Benefit Chicago” fund to pool its assets (including those from donor-advised funds) with assets from the MacArthur Foundation and invest that pool, totaling $100 million, into projects that benefit low- and moderate-income communities in and around Chicago.

In Grand Rapids, the city with the largest wealth inequality in Michigan, the Grand Rapids Community Foundation provided a $200,000 loan to a new loan fund that focuses on entrepreneurs who have been excluded from small business lending because of their income, net worth and other factors that often align with racial disparities.

In the Washington, D.C. metropolitan area, the Washington Regional Association of Grantmakers partnered with Enterprise Community Loan Fund to create the “Our Region, Your Investment” initiative, which provides loans to support tenants in purchasing their own affordable buildings in D.C., preventing those buildings from being sold to market-rate developers, most likely leading to displacement.

Credit: National Philanthropic Trust 2017 Donor-Advised Fund Report

In Philadelphia, earlier this year, The Philadelphia Foundation partnered with Reinvestment Fund to create the PhilaImpact Fund, a commitment to invest $30 million in community foundation assets into neighborhood development projects that support regional growth and local initiatives benefiting low- and moderate-income households throughout Greater Philadelphia.

“We have had donors come to us saying they wished there were more opportunities for this,” says Mark Froehlich, chief financial officer at The Philadelphia Foundation. “Foundations hold so many assets that have yet to be tapped for this type of work.”

People often give money to and through community foundations because they love the places they call home, and community foundations have oriented their entire operations around that premise.

“As a community foundation, we’re inherently place-based in our mission,” says Froehlich. “We put so much effort into making sure we’re spending those grant dollars well, that we’re supporting the region, making strategic decisions, but we understand there is so much more we can do with [the rest] that’s invested.”

But as much sense as it makes for community foundations to invest more of their assets into the communities after which they’re named, it’s not so simple in practice. The laws, regulations and informal customs governing community foundations are similar to those found in private foundations established by wealthy families or university endowments. Those laws, regulations and customs all typically require that the entity managing the philanthropic assets invest those assets responsibly, with a focus on optimizing financial return. It’s a concept known in shorthand as “fiduciary responsibility;” the idea is that following these protocols maximizes the amount that can be disbursed in grants every year.

The board of directors at each foundation has the final say when it comes to fiduciary responsibility. “We still have a fiduciary responsibility, so it was a board conversation and a board decision to open the account [at Self-Help Federal Credit Union] and make it available for the purposes that it’s available for,” says Elliott Balch, chief operating officer at Central Valley Community Foundation.

Time has been a key factor in moving more community foundation assets into more place-based investments. Time to educate board members and encourage them to learn about the potential to use both the grantmaking and investment sides of the community foundation to make a difference. And, even more crucially, time for entities like Self-Help Federal Credit Union or Reinvestment Fund to reach a point in their own life cycles that they’re positioned to pass the “smell test” of a community foundation board looking to judge the safety of its investment.

If you went back to 1980, when Self-Help was founded in North Carolina, many fewer organizations had committed to the specific mission to invest in historically marginalized communities. Those that did were generally very tiny — a credit union here, a community bank there. Reinvestment Fund wasn’t even founded until 1985, originally known as the Delaware Valley Community Reinvestment Fund.

Organizations like Self-Help or Reinvestment Fund would start to make real headway in the mid-1990s, thanks to a few key policy changes. One was the 1994 creation of the Community Development Financial Institutions Fund, or CDFI Fund, an arm of the U.S. Treasury that provides grants and other financial support to federally-certified community development financial institutions (CDFIs). One of the requirements for federal CDFI certification is that the entity, whether a bank, credit union, loan fund or venture fund, must have 60 percent of its lending, investments and other business in low-to-moderate income census tracts. Self-Help and Reinvestment Fund became two of the first federally-certified CDFIs.

Another key policy tweak was the new rules under the Community Reinvestment Act, put in place in 1995. The new rules emphasized that banks could meet their obligations under the Act by investing in or lending to federally-certified CDFIs.

With the CDFI Fund and the new Community Reinvestment Rules in place, federally-certified CDFIs started gaining traction all around the country. There are more than a thousand of them today, in all fifty states plus Puerto Rico and American Samoa. More importantly, some CDFIs, like Self-Help and Reinvestment Fund, started to grow larger. Bigger balance sheets and long-term track records of success are key to securing an investment commitment from a community foundation board.

Today, Reinvestment Fund has around $465 million in assets, having loaned or invested over $2 billion cumulatively since 1985. While it’s now financing projects all over the country, Reinvestment Fund remains committed to its home city: out of $203 million in new loans made in 2017, $62 million went to projects in and around Philadelphia. On top of all that, Reinvestment Fund is one of six CDFIs with a rating from S&P — the same ratings agency that Wall Street investors use to assess the risk of investing in corporations or state and local bonds. With an “AA” rating, Reinvestment Fund is rated as a safer investment than bonds issued by the states of Illinois, West Virginia, Pennsylvania, Michigan, Kansas, Connecticut, California, New Jersey or Kentucky.

Reinvestment Fund became one of the first CDFIs to use that rating to raise money Wall-Street style, going through a successful $50-million bond issuance last year, raising capital from mutual funds and pension funds the way corporations do.

“I’ve spoken with other chief financial officers, who have said it can be difficult to get approval for an investment fund like this,” says Froehlich. “Reinvestment Fund made my job easy, being so good at what they do, having that rating, having done a public bond issuance.”

Self-Help Credit Union in North Carolina and Self-Help Federal Credit Union (which has branches in California, Illinois, Wisconsin and Florida) hold more than $2.5 billion in assets combined. Self-Help has never lost a single dollar of any depositor since it was founded in 1980. Being a credit union also means being a regulated financial institution — the National Credit Union Administration (NCUA) regulates credit unions across the United States. In the same way the Federal Deposit Insurance Corporation (FDIC) safeguards banks, the National Credit Union Administration insures credit union depositors up to $250,000. In order to protect itself from having to pay out too much in insurance claims, the NCUA closely watches credit union bottom lines, seeking to prevent failure; the FDIC follows a similar protocol.

Given this backdrop, it was relatively easy for Central Valley Community Foundation to move some assets into a money-market account at the Fresno branch of Self-Help Federal Credit Union. The first $2.6 million was the easiest — that money came from donors who aren’t as concerned with growing their philanthropic assets over time through investing. Now that the community foundation has an established Self-Help money-market account, they can offer new donors the opportunity to have funds deposited into that account before granting them out later, and they can approach existing donors to see if they’d be interested in transferring previously donated dollars into the account.

“It was not a difficult conversation with the board,” says Balch. “For us, this is part of a range of investment options we offer our donors. From that perspective as a board member it’s not difficult as long as we are disclosing information, being transparent about providing options.”

Even with a track record of success over time, it’s not automatic that place-based foundations will suddenly start pouring money into mission-driven financial institutions with a focus on place-based investments. It has also taken resources — people, to be specific.

Every year, in places like San Francisco’s Fort Mason Center for Arts & Culture or big hotels in Chicago or New York, people with an interest in using finance and investing to address social issues — often calling themselves impact investors — gather to discuss their latest projects and pat each other on the back for a job well-done. Over the past two years, one of the regular faces at these conference halls and cocktail hours has been Annie McShiras, who also works at Self-Help Federal Credit Union.

The credit union hired McShiras to work the crowd at these conferences and cocktail parties, securing investments for their money market account or certificate of deposits. At times, it’s a frustrating job; most self-proclaimed impact investors gravitate to newer, sexier-sounding ventures such as a more efficient solar panel or an easier way to purify drinking water. But McShiras has found traction among a subset of those who come to these conferences and cocktail hours — community foundations.

“More and more we’re seeing community foundations pay attention to the ways that their investments are having an impact on the communities where they work,” says McShiras. “We’re seeing a shift in terms of those foundations wanting to align their investments with their values, and start making more impact investments or socially responsible investments with money that would normally be utilized for market-based investments.”

“In families that I’ve touched, you have generations of non-homeownership, then all of a sudden you have one person buy a house, and it seems that the rest of the family starts to buy a home. It happens a lot in our low-income families. Once they buy a house, it makes a ripple effect with the rest of the family members.”

Just last year, in addition to the Central Valley Community Foundation’s $2.6-million deposit, McShiras scored an $8-million deposit for Self-Help from the Silicon Valley Community Foundation, the largest community foundation in the United States (which currently faces its own #MeToo revelations).

Generally, McShiras begins conversations with community foundations that may already support the credit union’s free tax-preparation services, or its financial coaching and financial empowerment programs. Foundation grants may also support zero-interest loans for renewing DACA work/education permits, which cost $495; or for subsidizing naturalization fees, which, according to Pereirra, currently run around $1,000. Community foundations may already support downpayment assistance for homes, directly or indirectly connected to the credit union.

McShiras describes her approach this way. “Often [we] say, ‘we’re so happy to be working with you on the grant side of things, I want to draw your attention as well to this program we have called Mission-Supportive Deposits, where you can support the work that we do and make a good return on your cash savings by investing in our credit union through one of our cash investment options.’”

For foundations in the same community as one of the branches they invest with, such as the Central Valley or Silicon Valley Community Foundations, it’s easy to become a member organization and open up a deposit account. For those not based in a community where there’s a branch, it’s a bit more complicated.

“Also, because we’re a credit union, a member-owned financial institution, and we’re not paying outside shareholders, we actually pay a pretty decent return on our savings products that often beat out what some of those same investors are getting from big banks on long-term certificates of deposit or money-market accounts,” McShiras adds.

For bigger deposits that go well beyond the $250,000 deposit insurance limit, one key learning experience has been to understand the questions that community foundation boards may have about the relative risk of making a deposit larger than the insured amount.

As McShiras notes, being a regulated financial institution means being a safer investment than almost any stock or bond — just because they focus on the most vulnerable populations doesn’t mean they’re taking irresponsible chances, like a subprime mortgage lender. For 38 years, Fresno’s Self-Help branch has focused on how to make responsible loans to low- and moderate-income borrowers. The credit union’s delinquency rate, or the percentage of loans that are late or behind on payments, is just 0.86 percent, McShiras says. Other impressive numbers include the $2.5 billion in assets and 130,000 members across five states on both coasts and the Midwest.

“All of these reasons have helped make the case for investors like Central Valley Community Foundation to feel assured they’re making a safe investment above our insurance limit,” says McShiras.

Her job, while still frustrating at times, is getting easier. “Initially it was a series of questions we were getting from investors about what our risk profile is,” says McShiras. “Now, I make a proactive case.”

A while back, Balch tells me, a Fresno merchant left Central Valley Community Foundation a few hundred thousand dollars in cash after he died.

“He was a big parks advocate when he was alive,” Balch says.

That money has turned into dollars to rally voters around a local ballot measure, scheduled for later this year, to increase funding for parks in Fresno through a sales tax.

“It’s a few hundred thousand dollars we’re putting in, but we’re hoping over 30 years that it becomes a billion dollars of investment in the fabric of our community — parks, art, trails, after-school programs,” Balch says. “Where before we were making grants of five or ten thousand dollars for parks programs and music programs, we’re trying to turn that into a return thousands of times over.”

The foundation’s Self-Help investment fits right into that vision, according to Balch. The loans that Self-Help makes — for a family’s first home, or for a car that gets a parent to a better job to pay the mortgage — help to ensure that the people who will vote for that ballot initiative can actually benefit from the parks it would help build, as would subsequent generations of their families.

“What Self-Help is doing is providing maybe a family’s first access to decent credit for a reasonable home loan or car loan that’s not usurious,” Balch says. “And that home, when they’re not worried about having to move, that [becomes] a base of stability for that family’s kids, that’s going to take the parents’ minds off where are we going to live next week and put it on how do I read to my kid and make sure they’re getting their homework done. The kid can focus on getting some homework done. When we’re thinking about one generation to the next, those are the key moments.”

This article is part of The Bottom Line, a series exploring scalable solutions for problems related to affordability, inclusive economic growth and access to capital. Click here to subscribe to our monthly Bottom Line newsletter. The Bottom Line is made possible with support from Citi Community Development.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)

Next City is a nonprofit news organization that believes journalists have the power to amplify solutions and spread workable ideas from one city to the next city. Our mission is to inspire greater economic, environmental, and social justice in cities.

Learn more about us →

20th Anniversary Solutions of the Year magazine