On a muggy August Saturday, about a dozen East Harlem residents joined staff from the advocacy group New Economy Project and the NYC Department of Consumer Affairs for a walk around their neighborhood. A majority of the residents said they’ve lived in the neighborhood for decades, including three residents who claimed 50-plus years living in East Harlem. The gathering point was Union Settlement, which has provided a wide range of wellness and community programs for East Harlem residents since 1895.

Huddled in a circle, the group began to discuss how the neighborhood makes it easier or harder for residents to manage household finances. One resident brought up the credit union branch 30 feet away, inside Union Settlement . Others had heard about the branch, but some hadn’t realized anyone could go in and open up an account or apply for a loan—not just those who receive services from Union Settlement. On their way to the next stop on their walk, residents made a point of how much businesses have changed or moved around within the neighborhood. It can be disruptive for New Yorkers, many of whom don’t own a car.

The walking tour, or “Walk Shop,” as the New Economy Project called it, helped kick off a yearlong conversation with residents about the ways their neighborhoods affect financial health. The underlying question: If we thought about financial distress like a disease, something that infects a neighborhood and spreads sometimes in hidden ways, how could cities begin to fight back that disease on a neighborhood level?

The results of that yearlong conversation were revealed last month, with the release of a report from the Department of Consumer Affairs, detailing research findings and some results from pilot projects conducted in response to those findings.

Officials at the Department of Consumer Affairs Office for Financial Empowerment initiated the conversations in 2016 (see Next City’s earlier coverage). After years of building up the city’s network of Financial Empowerment Centers, which offer free financial counseling now to around 8,500 households a year in NYC, most of them low-income or households of color, leadership got curious about the limitations of the one-on-one counseling model. As many households as they were reaching, that’s just three out of a thousand NYC households a year—barely scratching the surface of how many are facing situations where a little bit of financial counseling could make a meaningful difference.

The city can’t force every household to come in for all the financial counseling they need. Nor could they believe, based on years of financial counseling experience and tens of thousands of clients, that every household is completely to blame for its own financial distress. Neighborhoods, the places where clients returned after walking out of Financial Empowerment Center doors, were a next logical target of inquiry.

“Neighborhoods matter,” says Debra-Ellen Glickstein, who has worked on financial empowerment for nearly two decades (and was executive director of the financial empowerment office when this project started last year). “It’s clearly not just up to the individual, there are systems in neighborhoods that enable or hamper economic success.”

Other researchers, like Raj Chetty, have shown time and again that zip codes matter in terms of economic and social outcomes. There is also more and more research every year looking into inputs—what it is about a given zip code or neighborhood that leads to disparate outcomes. In health, researchers have labeled these inputs, “the social determinants of health.”

What about for financial health? And out of the many factors in a neighborhood that could possibly affect financial health, what matters most?

Instead of paying a few consultants a couple hundred thousand dollars (or some academics a few thousand dollars) to come up with an answer, the agency put out an RFP in 2016 to community-based organizations in neighborhoods that were identified in an earlier study as facing high levels of financial distress. Each proposal laid out a collaborative team of organizations that could engage residents to explore how their neighborhood affects financial health. The winning proposals came from the New Economy Project and the Bedford-Stuyvesant Restoration Corporation (based in Brooklyn’s Bed-Stuy neighborhood).

Bed-Stuy Restoration Corporation was already a part of the city’s network of Financial Empowerment Centers, providing free one-on-one financial counseling for households in Brooklyn. For them, this project was a new way of working with the Office of Financial Empowerment.

“It was not just about reaching a hundred more people and how many more can we get in the counseling door,” says Tracey Capers, executive vice president for programs at Restoration. “It was really thinking about, what is an overall structure or system or environmental change we could help make in the neighborhood.”

The collaborative research teams found that “presence does not always equal access.” Like the credit union branch inside Union Settlement, some bank options in the neighborhood may come with perceptions that may or may not accurately reflect their true accessibility. A bank may require account minimums to avoid monthly fees, and those minimums may be too high. Even if there are newer, more affordable options available, word may not travel around the neighborhood very well, or a branch two or three blocks away may just be too inconvenient, especially if there is a check cashier location right along someone’s existing daily commute. Or people just may not trust a financial institution. Wells Fargo was not the first or the only large bank that made it a habit to prey upon its customers.

As an experimental intervention, New Economy Project worked with one of its partners, the Lower East Side Peoples Federal Credit Union, which owns the Union Settlement credit union branch, to create a “pop-up credit union” at the offices of LSA Family Health Services, a social services and advocacy organization serving primarily Spanish-speaking populations (East Harlem, also known as El Barrio, is majority Hispanic). At the pop-up credit union, residents could open accounts and receive bilingual financial counseling on the benefits of banking with a credit union. New Economy Project also trained a few residents to serve as “promotoras”, financial health promoters among their peers, modeled after health promotion workers used in other parts of the world (and also in the U.S.) to increase access to healthcare in low-income communities.

During the time of the interventions, January to March 2017, the credit union branch inside Union Settlement House reported it opened twice as many new accounts as it did in the same period the previous year.

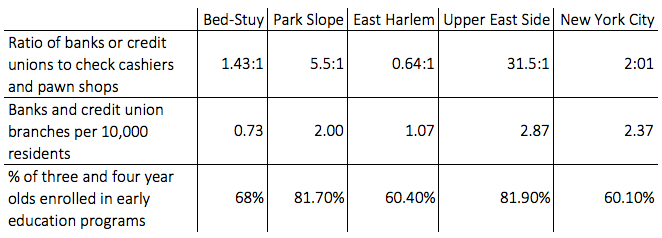

Another important important finding was that a relatively small slice of businesses have a direct and significant impact on a neighborhood’s ability to promote financial health. Those businesses are grocery stores, financial institutions, and childcare options. The research methodology combined resident-sourced qualitative data with quantitative data about Bed-Stuy, East Harlem, and two wealthier neighborhoods (Park Slope and the Upper East Side) for the sake of comparison, drawing from various public sources. Poorer neighborhoods like Bed-Stuy or East Harlem were more likely to have significantly lower ratios of banks and credit unions to check cashiers and pawn shops, and a significantly lower percentage of three- and four-year-olds enrolled in early education, for example.

Data from OFE's Neighborhood Financial Health Goals & Indicators.

On the qualitative side, in Bed-Stuy, the collaborative research team found that residents repeatedly identified lack of quality, affordable childcare options a major pain point and a source of stress on residents’ ability to keep jobs and secure income. Existing day care options are over-enrolled, can cost up to $2,000 a month, or may not offer hours that fit with parents’ busy work schedules and long commutes. Friends and family can help, but that resource also has its limits—friends or family may get a new job that takes away from their availability to help, or may want to start taking night classes to finish up a degree or a certification.

The childcare finding underscores that programs like the New York City Housing Authority’s Childcare Business Pathways, which supports public housing residents in properly licensing and operating their own home-based childcare businesses (see Next City’s earlier coverage), are badly needed. In Bed-Stuy, the research area included the housing authority’s Marcy Houses, meaning such a program could, for example, make a difference in terms of neighborhood financial health by prioritizing any future applicants from that development.

The Office of Financial Empowerment and its partners expect these and other insights from the research to help guide follow-up work. The agency has even added a staff member for a new position focused on community wealth building.

“It was a really great project for everyone to work on the ground and really learn the patterns from the neighborhood in new ways,” says Capers. “The findings weren’t fully surprising, but it was helpful to have a spotlight shined on it and we will likely use those findings to strengthen our other work.”

UPDATE: This article has been changed to clarify where the New Economy Project works and where promotoras have worked to increase access to healthcare.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)