An increase in black-owned businesses could lead to better economic outcomes in marginalized communities — including improved job creation and, according to at least one statistical analysis, lower rates of violent crime among youth. “The more black-owned businesses are present, the more they may be serving as role models as well as providing access to capital,” sociologist Karen Parker told me in December 2015, when a report was published that she authored on the connection between black entrepreneurship and a drop in crime in U.S. cities. But reaching more black entrepreneurs, both current and potential, is fraught with historical and structural barriers, as evidenced by Small Business Administration data.

(Credit: Expanding Black Business Credit Initiative)

Spurred in part by the poor performance of an SBA loan program in reaching black-owned businesses, last week the Expanding Black Business Credit initiative (EBBC) released a report and a proposal to deepen and expand upon the work of supporting economic liberation for black communities. (Fittingly timed to Juneteenth.)

The year-old EBBC consists of 11 lender or investor organizations, including eight CDFIs (community development financial institutions), a majority of which are black-led. The new report combines evidence and arguments for further investment in black-led CDFIs as a key strategy for increasing access to capital for starting and growing black-owned businesses.It’s EBBC’s hope that black-led CDFIs can serve as a “beachhead” for other investors, spreading best practices about how to make successful investments in black-owned businesses and ultimately creating a “viral impact” for investing in black-owned businesses.

“If the investments and success are large enough, then other intentional mainstream investors may get involved leading to a cycle of success for both investors and low-wealth Black communities,” the report reads.

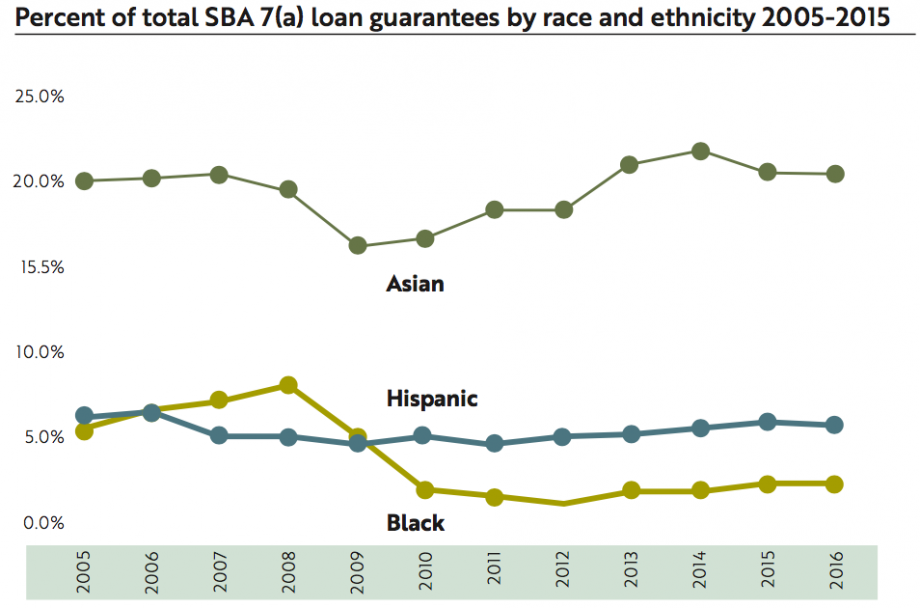

The report notes that the focus is not to take away from Latino-owned businesses or Asian-owned businesses, but EBBC believes each of these markets has unique challenges that warrant unique initiatives that should stand on their own, and the history of slavery and repeated structural violence against black communities in the U.S. warrants that black-owned businesses get top priority.

Firstly, there’s the wealth gap: The median net worth of white households is $132,483, compared with $9,211 for black households, according to the U.S. Census Bureau. That means hardly any capital available from “friends and family” for the average black household, a crucial source of runway capital that’s often expected before coming to a bank for a small business loan. Lack of wealth also means lack of collateral, which contributes directly to the credit gap; the Association for Enterprise Opportunity (AEO) estimates there are up to $8.5 billion in unmet capital needs for black-owned businesses. In its report on the state of black business in America, AEO adds the trust gap, referring to the history of mistrust and implicit bias that keeps mainstream financial lenders from reaching black-owned businesses.

“[Black business owners] don’t go to financial institutions and banks to actually seek capital anymore, because they already feel they’re going to be turned down,” AEO’s CEO Connie Evans has told me previously.

EBBC believes that black-led CDFIs, while not perfect, are best positioned to reach black-owned businesses in large part because they can more easily bridge trust gaps and overcome any implicit bias between borrower and lender. “We have found that black-led CDFIs are particularly adept at seeing past negative perceptions to understand and unearth hidden value,” the report reads.

While lending to many black-owned businesses does often require extra support in terms of technical assistance, the report gathered data to show that the financial performance of black-led CDFIs is similar to other CDFIs. For the data analysis, the group worked with Aeris, which provides third-party independent ratings of financial health and social impact for CDFIs. They analyzed seven CDFIs (which requested to remain unnamed) with a total of $630 million in assets. The data show repayment performance across the group was on par with or better than industry benchmarks despite lending disproportionately to black businesses in their geographic region.

(Credit: Expanding Black Business Credit Initiative)

Despite that track record, black-led CDFIs have had difficulty raising more capital to reach more black-owned businesses or invest greater amounts in any given black-owned business. It’s the racial equity double-edged sword: Black-led CDFIs are better at reaching black-owned businesses, but due to the same racial issues their borrowers face, black-led CDFIs end up having their own difficulty raising capital.

“Many of the CDFIs who have been most successful at lending to black businesses are black-led small businesses themselves and so suffer from some of the same negative perceptions when they try to raise capital,” the report reads.

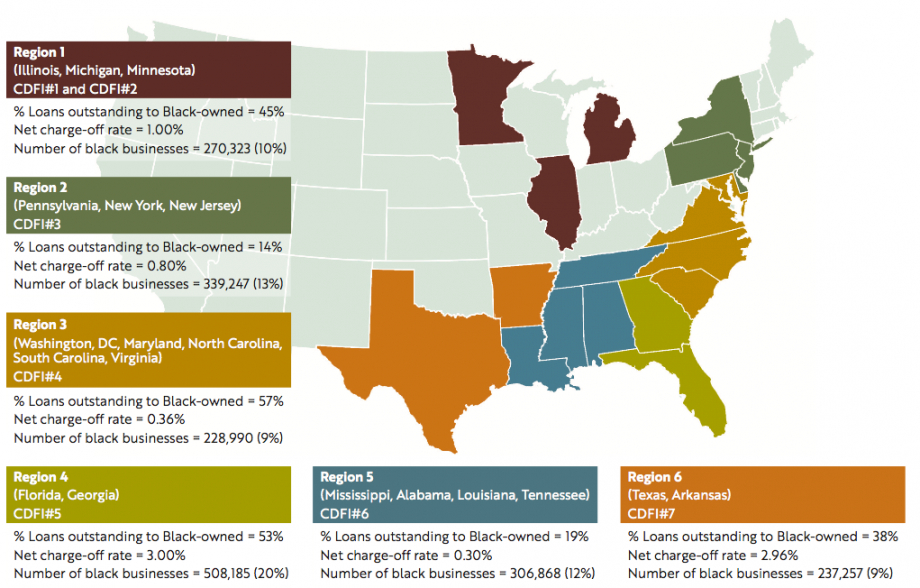

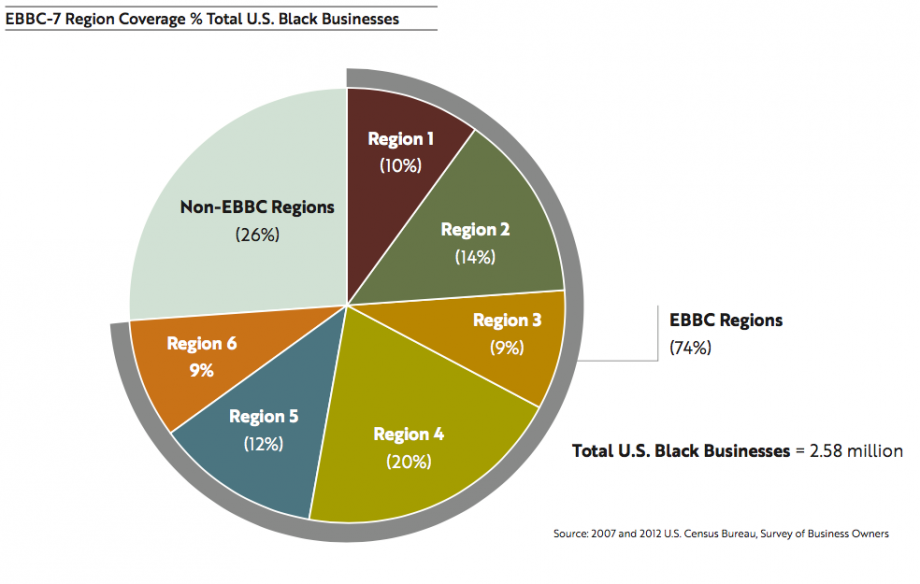

As a group, the EBBC’s goal is to create a national peer network of organizations that learn from each other and raise capital collaboratively. The structure of the investment vehicle isn’t finalized, but they plan to engage banks (motivated by the Community Reinvestment Act), foundations, wealth management firms, and high-net-worth individuals and families. The proposed vehicle would support black-owned businesses with at least five employees and more than $1 million in annual revenues, in both urban and rural areas. Seven regions were chosen strategically, covering 74 percent of black-owned businesses in the U.S.

(Credit: Expanding Black Business Credit Initiative)

The group envisions seven to 10 black-led CDFIs or other lenders being part of the peer network, receiving the investment as a group and sharing lessons among each other as a group. The EBBC took inspiration from the Housing Partnership Network of affordable housing organizations, which has collaboratively launched multiple initiatives to raise capital and support work in that sphere.

“Success will come through careful scaling of each organization,” the report reads, “but the real success of the program will come with successful communication of outcomes to a broad audience of other lenders in each region.”

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)