There’s an 86-inch flat screen TV facing out the big front window toward the outdoor seating area at IV Purpose (“for purpose”), a Black-owned sports bar and restaurant in Brooklyn that opened in July 2020. It looks out onto Fulton Street — the main drag through Brooklyn’s historically Black but contentiously gentrifying Bedford-Stuyvesant.

During a summer that featured a historic NBA playoff season hosted inside a “bubble,” IV Purpose co-owner Darnell Joseph says it turned out to be the safest and sometimes the loudest place for the neighborhood to enjoy games and other events together, a welcome change after several months of social isolation.

And it very well might be the best — or at least the most entertaining — embodiment of a new chapter in the history of Black credit unions.

The three IV Purpose co-owners have known each other since at least their high school days in Bed-Stuy. In 2019, they decided to pool their savings and open up a sports bar. There aren’t very many in the neighborhood, none really along this stretch of Fulton Street.

They found an ideal location, close to a subway stop, a former two-story restaurant space but it needed a lot of work. It had been vacant for so long that the unit had its gas meter removed — and unfortunately, due to a political tussle involving former NY Governor Andrew Cuomo, there was a temporary moratorium on new gas meter installations until November 2019. Obtaining a liquor license added more delays. Finally, IV Purpose was ready to open — on March 17, 2020. On the day before, NYC ordered all bars and restaurants temporarily shut down due to the pandemic.

The business burned through a lot of cash for construction and other pre-opening costs, but it wasn’t eligible for the first round of Paycheck Protection Program loans, which were based on businesses’ payroll for 2019 or the first two months of 2020. Since IV Purpose hadn’t opened, it didn’t have any payroll. Pandemic or no pandemic, cash flow challenges are still the most common reason any small business closes.

But Joseph was able to secure a $50,000 loan from Concord Federal Credit Union, based nearby at one of the oldest historically Black churches in Brooklyn. Most of the loan went to cover payroll for IV Purpose’s newly hired workers. The rest went to things like the big screen TV and thousands of dollars’ worth of PPE and air purification equipment — all contributing to keeping the doors open and growing a business that could eventually support even more workers. IV Purpose now has 18 full-time or part-time staff, Joseph says.

That loan came about as a result of a dramatic shift in the credit union’s business model, a shift initiated through a partnership with Inclusiv, a national network of credit unions that focus on community development. With Inclusiv’s help, Concord expanded its eligible membership, modernized its technology and hired its first full-time staff since it was established in 1951.

As a result, Concord Federal Credit Union has nearly tripled its loan portfolio since the beginning of the pandemic. Meanwhile, Inclusiv is now working with 80 majority-Black credit unions across the country, and some are experiencing even more significant transformation in their lending or membership.

“I didn’t know there was a credit union at the church,” Joseph says. “But they are definitely one of the cornerstones of the community.”

Across the country, there are around 260 majority-Black credit unions, according to the National Credit Union Administration, the federal agency that regulates credit unions and insures their deposits. That’s down from 389 majority-Black credit unions in 2013, the first year the NCUA’s Office of Minority and Women Inclusion submitted its first required annual report to Congress. But the fall in numbers isn’t unique to Black credit unions — there were 6,681 federally insured credit unions overall in 2013, compared to just 5,231 today.

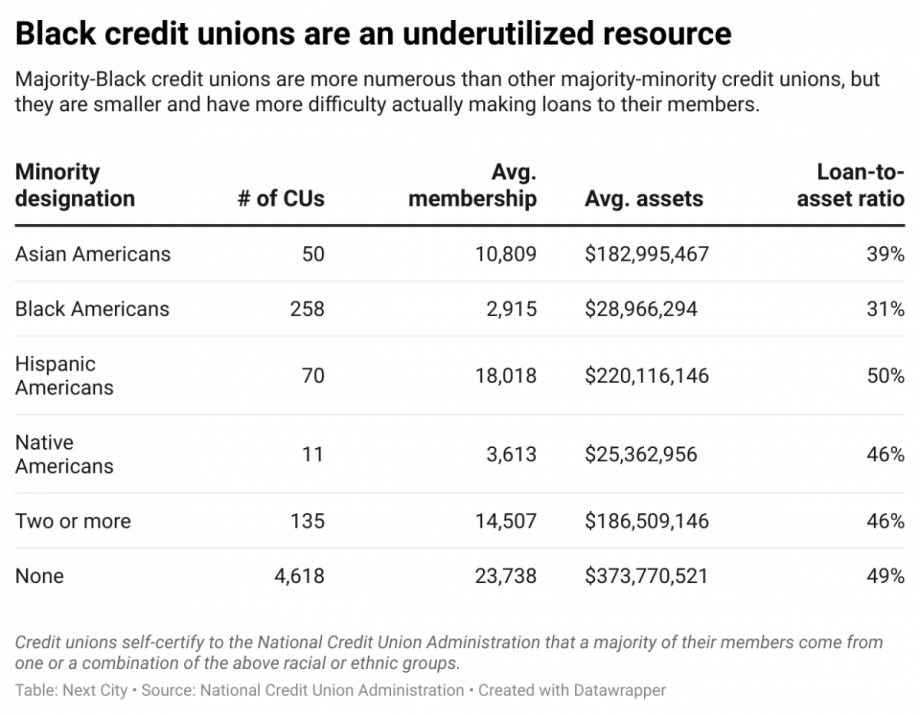

Though their numbers have dwindled, there are still more majority-Black credit unions today than there are majority-Latino, majority-Asian, and majority-Native credit unions combined. But even though credit unions have long been more common among Black communities versus other racial or ethnic minority groups, majority-Black credit unions are typically smaller and have more difficulty lending out to their own members than other credit unions with a minority-designation from the NCUA.

Industry-wide, credit unions have an average loan-to-asset ratio of 49.1% — that’s the percentage of their assets that are actual loans to members, not just treasury bonds, municipal bonds, stocks or other investments. Majority-Black credit unions have the lowest loan-to-asset ratio of any group of minority-designated credit unions — just 31.1%.

There are multiple reasons why that’s the case. A lot of it goes beyond the credit unions themselves.

Like their commercial bank counterparts, credit unions are subject to intense scrutiny of their lending practices by federal regulators. Those regulators evaluate every loan made by the institutions they oversee, examining factors like loan-to-value ratios — if a loan is equal to anything more than 60% or 80% of the value of the underlying real estate, depending on the kind of real estate, regulators start asking more questions. The same regulators oversee Black credit unions as all other credit unions.

That’s why it matters so much that there is now more and more evidence coming out about racial bias in the real estate appraisal process. A house may need $100,000 in rehab work, but that house will appraise for a lower value just for being in a Black neighborhood versus a white neighborhood — that may mean the lender makes a smaller loan that doesn’t cover all the necessary work, or the loan may not happen at all.

Borrowers’ credit scores are another typical item that regulators scrutinize. The racial bias in credit scores is well documented.

And many majority-Black credit unions just weren’t built to make loans — in a world still full of financial institutions that make a business out of preying on Black communities, many Black credit unions were built mainly as a way for members to have a trusted place to deposit their savings.

That’s especially true of credit unions attached to Black churches. Many majority-Black credit unions have only part-time staff, or they’re run by volunteers from a church congregation. They’re open for business maybe two days a week, sometimes only one day — Sunday of course, when members could stop by before or after services to make deposits or withdrawals.

Established in 1951 to serve the members of Concord Baptist Church, for its first seven decades Concord Federal Credit Union had zero full-time staff. Before the pandemic it was only open on Sundays and Thursdays. Today it has two full-time staff and is currently looking for a third.

Chief Operating Officer Carolin Lopez was the first full-time hire at Concord Federal Credit Union. She came on board at the end of 2020, bringing with her 15 years experience working in credit unions. In her previous position with a credit union in New Jersey, she helped create and run a series of “remote” branches inside Head Start Program locations, providing access to financial services but also financial counseling to parents of participants in the early childhood education program for low-income families.

Denise Michaux came onboard as CEO in early 2021, a banking industry veteran, longtime member of Concord Baptist Church and previously a board member at the credit union.

“In the past, before our time, they were more into the savings side of it,” Michaux says. “With Carolin and myself coming on board, we really had to put the emphasis on lending.”

Inclusiv began working with Concord in 2018, under an initiative it now calls “Inclusiv/Black Communities.” As I reported on previously, that work began with updating the credit union’s back-office technology for accounting, processing and compliance; adding debit cards to its services for members; and also expanding its field-of-membership, which was previously limited to members of the church’s congregation.

Since Lopez and Michaux came on board they’ve also added ACH — the ability to wire payments to and from accounts at all other financial institutions, allowing for auto-pay and other services now considered basic essentials for any depository institution.

And they’ve put the marketing in hyperdrive — Lopez has been visiting local businesses, like IV Purpose, carrying a secured laptop that she can use to open up new accounts right on the spot. The credit union’s new website was designed by a Black firm and uses photography featuring actual members of the credit union itself.

Word of mouth is still a big marketing component, but it seems to already be showing results. Joseph says since he took out his loan, he’s referred multiple friends and family who have since taken out loans from Concord. Lopez says most of the loans through the pandemic have been for debt consolidation, some major appliance purchases, or school loans.

“When I first found out about the [credit union], I tried to tell a lot more people about it, but they didn’t think it was real at first, they thought it was a scam,” Joseph says. It wasn’t till after he took out a loan himself that others saw it was for real, he says.

The credit union wasn’t an SBA lender before the pandemic, but Lopez says it did eventually do 14 Paycheck Protection Program loans, most for around $14,000 — including one to IV Purpose in the second round of PPP loans, after the bar finally had some monthly payroll numbers to show.

To help pay for all the new technology, marketing and full-time staff salaries, Concord has also gotten support from Inclusiv in the form of a grant as well as help applying for financial support from others — NY state’s economic development agency, the U.S. Treasury’s Community Development Financial Institutions Fund, and even the NCUA. The credit union has received six grants from outside sources since 2019, infusing Concord with close to $1 million.

The full impact of those grant dollars, not to mention Inclusiv’s support, won’t be known for a few years at least, as Concord continues to ramp up its lending. It’s a bit of an extreme case — even after tripling its loan portfolio since the beginning of the pandemic, Concord’s loan-to-asset ratio is now just under 15% — still far below the industry average. As that ratio improves, it also means the credit union’s revenues from lending grow, hopefully to the point where it doesn’t need grant support to stay open.

Out of around 260 majority-Black credit unions, around 200 have a loan-to-asset ratio below the industry average, including 80 with a loan-to-asset ratio below 20 percent. If majority-Black credit unions as a group had a loan-to-asset ratio equal to the industry average, it would amount to $1.3 billion more in loans to their members, according to a Next City analysis of NCUA data.

With funding from Citi and JPMorgan Chase, the Inclusiv/Black Communities initiative is now working with around 80 majority-Black credit unions across the country, says Monica Copeland, who leads the initiative. (Citi also provides funding to Next City for The Bottom Line.)

Like Concord, Copeland says those credit unions often have the deposits to support more lending to their communities. Even in the face of systemic racism that still stands in their way, these majority-Black credit unions see opportunities to connect with new borrowers who others have left behind, like Joseph and his new sports bar.

“They are a resource that is a hidden gem,” Copeland says.

Editor’s note: We’ve corrected Darnell Joseph’s name.

This article is part of The Bottom Line, a series exploring scalable solutions for problems related to affordability, inclusive economic growth and access to capital. Click here to subscribe to our Bottom Line newsletter.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)