Are You A Vanguard? Applications Now Open

In 1978, three real estate developers in Boston set their eyes on a decaying waterfront property south of downtown. The lot, owned by the bankrupt Penn Central station, was up for $3.5 million. The deal fell apart. A few years later, one of the trio, Frank McCourt, bought the land for around three times the rate and set up shop on the 24 acres, using them mostly as a parking lot. He and his wife became the largest private developers in South Boston.

In the coming decades, state and city leaders made a series of heavy infrastructure investments stretching into the McCourts’ acres. They broke ground on the Central Artery and Tunnel, a $14.6 billion highway project known as the Big Dig, and launched the Silver Line, a massive bus rapid transit operation that put a station at the center of the property. Frank McCourt contributed $25 million to fund the station project, but only after the city reimbursed him $30 million for the land that was seized. And after McCourt, in an eminent domain suit, won an additional $57.5 million.

McCourt was not just a real estate guy. He was a baseball fan. In 2002, the grandson of a one-time Boston Braves owner attempted to buy the Red Sox and move them south, to the land on the waterfront. When his bid failed, he quickly put the property on the market. Then he bought the Los Angeles Dodgers. He sold his waterfront acres for more than $200 million. Even if McCourt didn’t build the baseball field of his dreams, it’s fair to say he made a killing on the attempt.

For diehard fans of Fenway, the botched bid was a disaster narrowly missed. Yet the city also missed something significant with McCourt’s departure. A hefty chunk of the nearly $190 million he made on the sale of his waterfront property came from the improvements to his land backed by the city and by taxpayers. Had the government operated differently, it could have claimed some of the value it helped create on McCourt’s property as its own. It could have deployed value capture, the principle that the economic gain generated by a public policy — a zoning change or infrastructure investment — should make its way back to the public.

As the gap between the infrastructure our cities need and the money we have to fund it continues to widen, more cities are aiming to avoid their own McCourts. And value capture, an idea long en vogue with economists and policy wonks, is now starting to bleed slowly into City Halls, changing the way we pay for our cities.

More than a century before McCourt bought his waterfront property, Henry George, a Philadelphia-born economist, was scripting a philosophy that applies aptly to the Boston developer. All taxes, George argued, should be scrapped and replaced with one: A single tax on land.

For George, the way private owners profited from their land — enjoying huge gains through no actions of their own — was the source of all wrongs. “From this fundamental injustice,” he wrote, in 1879, “flow all the injustices which distort and endanger modern development.” His notions would flow directly to economic strategies in Amsterdam, where the government intentionally owns much of the land, and, via a less direct route, to emergent city-states like Singapore, where the government own the land and extracts any value added onto it.

George’s ideas have been a tough sell in his own country, where fierce property rights remain embedded in the culture. Though he never advocated for public ownership of land, but rather believed that privately owned land should be taxed differently, George’s notion of sharing costs for public benefit still rang of socialism to a populace raised to aspire to the American dream of home ownership and self-determination.

Yet the Philadelphian’s ideas attracted some surprising defenders. Milton Friedman, the Nobel laureate and progenitor of free-market economics, once conceded that “the least bad tax is the property tax on the unimproved value of land, the Henry George argument of many, many years ago.” George also had a solid backing in his home state. Since 1913, more than 20 Pennsylvania municipalities have turned to a two-tiered taxing system, one that charges for land at higher rates than properties. In Pittsburgh, the largest city to employ the strategy, the council hiked the land tax to six times the property billings, in 1989. Eight years later, a review of the city’s practice concluded that it churned out revenues with “no damaging side effects on the urban economy.”

Even so, in five years’ time, the city’s unique tax structure was ended, as wealthy homeowners outmaneuvered downtown developers and poorer residents to strike it down. Those two disparate parties who stood to gain from the system, but failed to defend it, reflect the somewhat unlikely coalition of progressive urbanists and real estate developers forming around value capture proposals. Advocates on the left push for smart growth, additional infrastructure and extensive public benefits, while real estate developers crave more density and fewer harnessing regulations. But what both agree on is a need for new mechanisms to pay for this development. And economists of all stripes often agree that taxing land, rather than the improvements put on the land, generates more profitable, equitable growth.

Indeed, land is finite. Boston can change, desert or develop its waterfront, but it cannot add more waterfront. This fact makes a tax on land ownership more efficient than a property tax based on the value of improvements, because there is no way for a land owner to retain land while avoiding taxes and, therefore, no incentive to sit on land without adding to its value. Now, landholders like McCourt can sit on swaths of undeveloped land, waiting for its worth to rise. As they wait, they send development sprawling. But a tax on the land itself, rather than on properties, would prod landowners to build frequently and densely. In economist parlance, a land tax results in less “deadweight loss” than a property tax.

Despite the evidence in its favor, the U.S. is far from applying a single land tax, and it is unlikely most communities will ever do so. Yet that hasn’t stopped a tide of other alternate tax policies from gaining popularity — strategies like those championed by George, intended to extract private money for public use. These include impact fees, licensing levies, inclusionary zoning policies, special assessment districts, tax-increments and a laundry list of other public financing tactics.

“We actually do a lot of value capture in the U.S.,” explained Gregory K. Ingram, president of the Lincoln Institute of Land Policy. “We just don’t use that term.”

For models of what further value capture could look like, advocates often turn south.

Early this morning, a trader sat behind his desk in São Paulo to watch prices. While the names and numbers varied, the types of companies, commodities and stocks he saw were little different than those his counterpart in New York tracked. Then a unique ticker passed by: One for Certificates of Additional Construction Potential, or CEPAC.

The notes, sold by municipalities, are one of the world’s most innovative public financing techniques. Across many sections of São Paulo, if a developer hopes to build or do nearly anything with her property — adjust its uses, expand outward or upward — she must first buy a CEPAC.

Value capture seeped into Brazilian politics as early as the 1970s. The concept that the value from policies should extend beyond private beneficiaries was written into the Constitution in 1988, and cemented into law in 2001. In approved districts, called joint urban operations, funds raise by CEPAC go toward neighborhood improvements. By 2008, São Paulo had approved nine such districts.

After a slow start, the certificates began selling. And the improvements began breaking ground, with millions spent on city streets, sidewalks, sewers, community facilities and parks. In a recent April CEPAC auction, the city raised $420 million, in U.S. dollars, to add onto its estimated $2.5 billion from prior auctions.

“They’re essentially selling zoning changes,” explained Ingram. Crucially, the building fees have not eaten away at developers’ profits. By some accounts, the rates of return for real estate in the districts increased.

A similar sentiment reigns in the United Kingdom, where value capture has long been woven into land use policy. Profits propelled by government action there are dubbed the “unearned increment” — benefits the public generated through its intervention, but has yet to claim.

Although the city did not reap the full rewards of McCourt’s land, Boston is closer to the British land use model than other metropolises. It is one of two major U.S. cities to deploy linkage fees, marginal payments that developers pay in exchange for the right to expand. Downtown, the city launched its first business improvement district (BID), where fees from private sources in its borders go toward small infrastructure improvements, in September 2010. While BIDs are increasingly common in cities nationwide, the Downtown Boston BID extends beyond the usual street cleaning and quality of life responsibilities to help support capital projects and infrastructure improvements.

Anthony Pangaro, one of Boston’s most prominent developers, is a high-profile supporter of the BID. His company, Millennium Partners, was behind two new luxury hotels downtown and scores of other properties.

“The money is now flowing,” he said of the BID, “and being spent on services, which are, in their nature, over and above what the city was able to do.” For him, the returns on involvement in the BID are similar to those for Brazilian developers. “In our view, it’s absolutely worth paying extra for.”

“Every day, developers turn to City Hall for approval of a project they expect to turn a profit.”

It’s not all that surprising that Boston’s West Coast counterpart on the value capture train is San Francisco, another robust urban economy with a history of bold public policy. The compact metropolis, tucked in the Pacific, is light-years ahead of others in value capture plans.

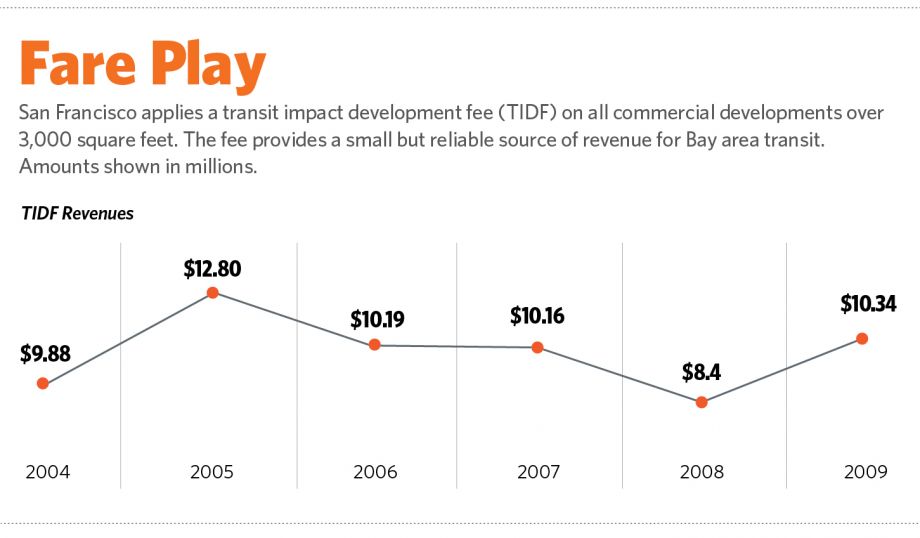

Beginning in 1981, the city has levied fees on any developer wishing to expand across non-residential space over 3,000 square feet. Decades later, the city went further, embedding the practice into residential development and city planning. In 2003, the city outlined its Public Benefit Zoning, requiring property owners to contribute to neighborhood improvements after beneficial re-zonings.

Despite the national economic downturn, the city has held strong. In four years, it expects to host nearly twice as many jobs as it did in 2005. Every day, developers turn to City Hall for approval of a project they expect to turn a profit. “The amount of growth that they are planning for in the next 20 years is mind-boggling,” said Evelyn Stivers, field director of the Non-profit Housing Association of Northern California.

Much of the growth comes with plans that resemble value capture. But the development, driven by real estate as always, will continue to bring something else. In several neighborhoods across the city, longtime residents are being steadily displaced as gentrification edges in and rents skyrocket.

In its plans, the city aims to seize some of the private value re-zonings create. Yet affordable housing advocates, like Stivers, are working frantically to ensure that residents are still around to receive it.

Uptown, a neighborhood on Chicago’s north side, is also gentrifying, but at a pace well behind its San Francisco peers.

Historically, the Chicago blocks have served as a landing ground for new immigrant arrivals. With that history, the area’s population is more diverse than surrounding neighborhoods, but also less stable — household incomes are lower and crime rates higher. With these deep challenges, Uptown is an example of a neighborhood that could greatly benefit from development, if the wealth created was channeled back into the community rather than into the bank accounts of a few private individuals or companies.

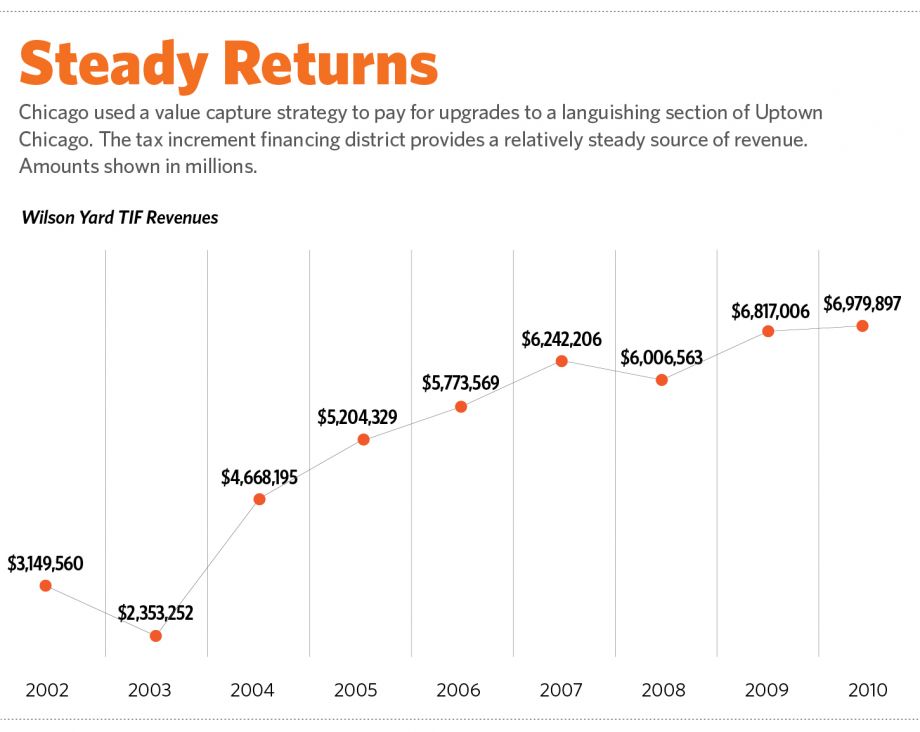

An immense Target store recently opened in Uptown’s center. Its subway stop, once dubbed the “crustiest and most rotten” station in the city, received a massive facelift. To pay for the makeover, the city turned to tax-increment financing (TIF), declaring the 144-acre Wilson Yards a TIF district in 2001.

Once a TIF district is marked off, the property values are frozen for a determined period — in Chicago, usually 25 years. The incremental gains are then thrown into a pot used to finance infrastructure. The pot goes to paying back bonds issued for development or directly for services that improve the value of the land and, in turn, the properties on it. According to figures from the Mineta Transportation Institute (MTI), the Wilson Yards TIF brought in close to $47 million in its first decade.

TIFs are perhaps the most common value capture tool used in U.S. cities. And along with their cousin, special assessment districts, they’re also the most fruitful. An MTI report claimed the revenues generated by the pair of mechanisms are the highest of any value capture tools used nationwide.

Despite the popularity of TIF in national policy circles, the response in Chicago has been more ambivalent.

“It’s definitely getting nicer,” said Nickolas Pappas, a lawyer who lives in Uptown and operates a private practice there. His office, across from the new Target and spruced-up subway, sits on a street that still resembles an older Uptown. Aging storefronts stand behind iron gates. Packs of homeless adults gather under awnings in the afternoon sun. Last winter, a hostage situation broke out down the block. Pappas recently moved his office up from the ground floor to escape the constant commotion. Around the corner, new condos priced to sell at $220,000 stand across from methadone clinics.

“Most of the people who move in aren’t from here,” Pappas said, detailing how new neighbors, from outside the city, come in expecting rapid renewal. To him, they’re naïve. He mentioned Logan Square, a nearby neighborhood that has pushed improvements for decades but is just now seeing them. “Things don’t change that quickly.”

The city hopes it can prove Pappas wrong, using the Wilson Yards TIF to ignite brisk growth. Behind its strategy is an economic logic that, again, emerged from Latin America.

In 2000, Bogotá implemented an expansive bus rapid transit network. Since then, several studies have shown that property values tick up as they approach stops along the line. To pay for the system, the city levies betterment contributions, asking owners to pay in advance for the increased value their property will attain.

“The lesson of the experience in Bogotá is that the payments work,” argued Ingram of the Lincoln Institute. In his mind, they work largely because they are funneled into local public goods — tangible improvements, like a sidewalk repair or streetlamp installation. “People are wiling to pay for something they can see in their neighborhood,” he said.

But in Chicago, that sightline is often hazy.

Launched in 1984 by then-mayor Harold Washington, TIFs took off under Richard M. Daley. By his departure, last year, the 22-year city chief had amassed 166 districts.

As they accumulated, the financing tools faced a growing wave of criticism. One common critique is that TIFs are merely “zoning for dollar” — plans that shuffle retail from one area to another, rather than spur citywide growth. Chicago TIFs, in particular, stand accused of favoring one section of the city over others. Written into the tools are a “but for” provision: Districts are only intended to lure private development into areas it otherwise would not go. Chicago created districts and directed dollars overwhelmingly downtown. And did so well after the area could expand but for the districts.

But the biggest broadside against the Daley-era TIFs zeroed in on their lack of transparency.

“Very seldom do the local residents have much of a sense of where the money goes,” explained Larry Bennett, a political scientist at DePaul University.

The issue became so significant that several aldermanic candidates recently ran on TIF reform, one calling for the abolishment of TIF districts altogether. Shortly after his inauguration, new Mayor Rahm Emanuel unveiled a major TIF revamp. For Bennett, the plan is unlikely to change anything. “I’m not terribly impressed with it,” he said.

Yet critics like Bennett see the Wilson Yards TIF as a success. It included provisions to maintain affordable housing while still spurring growth. “From a social equity perspective,” he said, “it was pretty good.”

If the Wilson Yards TIF prompts a flourishing Uptown, it would be an exception. Much of the financing scheme’s success arrived around the Magnificent Mile, an upscale stretch of retail and commercial bounty. In many regions of the city, the property values across a TIF district have accrued little over decades.

Chicago’s story points to a critical limitation of value capture policies: They depend on growth in a city’s economy and housing market. To capture resources, there must first be resources.

In a recent report on Brazilian land use, researchers admitted that the success of the CEPAC mechanism in São Paulo “demands not only a buoyant real estate market but a robust financial market as well.”

Our buoyant market in the U.S., during the housing bubble years, allowed some cities to implement a particular strain of value capture. As developers reaped gains from relaxed or adjusted zoning, municipalities began to pressure private real estate to return some of their windfall profits.

Inclusionary zoning, which requires that portions of development be affordable, emerged prominently in New Jersey, although it has stalled in the face of political opposition. In San Francisco, the dot-com bubble offered inclusionary housing a viable shot. On top of its linkage fees, the city was able to secure 1,328 affordable units from 1992 to 2008.

Across the Bay, Berkeley is also considering additional ways to procure private dollars for development. In one plan, developers pay into a city coffer in exchange for a benefits package — lifted building restrictions or less red tape. Details on the packages, fees and size of infrastructure investment are still being sketched out, explained Mayor Tom Bates.

The city can sketch these plans, he emphasized, because it is desirable to do so. “Every year we get 5,000 new students,” Bates said. “The rental market has been particularly strong. The vacancy rate has been very low.”

A few miles south, another city hosts a much less idyllic real estate market.

On a recent Friday evening, streams of pedestrians strolled through the Oakland “art murmur” — a gallery walk that showcases the city’s unique blend of established communities with its emergent pockets of new immigrants, artists and young professionals. A dozen blocks away sits is Lake Merritt, a stately urban park, where the city has plans to upgrade the regional transit stop. Around the lake are patches of office and apartment buildings, few of which top the trees. The city has room to grow.

But bringing private developers to the city is incredibly onerous, so much so that its council remains deeply reluctant to ask real estate developers for anything. They fear it will shun them away.

“Oakland is so desperate for development,” said Stivers, explaining that city officials believe, “asking a developer to do anything would just break the housing market.”

Unlike its neighbors in the Bay, the city has not approved any inclusionary housing programs. In part, that’s because a bulk of the housing units are already cheap. Land in Oakland has yet to generate an unearned increment. To spur development, in addition to the Lake Merritt plans, the city has upzoned its downtown and Chinatown districts.

Yet without a strong market, the city will face an uphill battle in procuring private financing, explained Nico Calavita, a leading expert on inclusionary housing policies at San Diego State University. “Even with upzoning,” he wrote in an email, “if the units cannot sell at prices that allow the recovery of all the developer’s costs, plus profit, there can be no land value recapture.” A similar fate faces other lagging Bay Area cities, such as Richmond or Vallejo.

Still, as rents continue to rise in San Francisco, Oakland is steadily drawing in newcomers. Development will soon arrive, and once it does the city will have a hard time obtaining private contributions to create more.

“What they have done,” wrote Calavita of the city, “is to make it impossible to ask developers [to] pay for public facilities and affordable housing” — at least, he added, until housing prices rise significantly.

In many ways, it’s appropriate that innovative development would hit a wall in Oakland. The city was the birthplace of the most significant chapter in economic development in California. A chapter that recently closed.

As Josh Stephens documented in the inaugural Forefront story, the California redevelopment agencies essentially “minted money” for cities. In January, Gov. Jerry Brown abruptly pulled the rug from the state’s floor.

“It’s still a pretty fresh wound,” said Susan Riggs Tinsky, executive director of the San Diego Housing Federation, in June. “The last six months have all been about unwinding and trying to think of the implications.”

When the agencies were unraveled, TIFs were essentially outlawed. City officials looking to use value capture tools have had to get more creative. On top of its linkage fees, San Francisco has begun accepting in-kind contributions for zoning changes or expediencies. A Whole Foods downtown will pay for its expansion that way. The city also has Mello-Roos districts, another levy tool, and infrastructure finance districts, regions that can be birthed outside of the redevelopment zones. But implementing those, explained Peter Cohen of the Council of Community Housing Organizations, is “very cumbersome.”

For city governments, these tools are also sub-par.

“I love TIFs,” said José Campos, from the San Francisco Planning Department, before correcting himself. “I loved TIFs, because of the whole concept of claiming the plan, claiming the vision.” For much of its history, urban development has meant destruction — tearing down blight, leveling decrepit buildings. Campos went on: “But TIF requires added value. You have to keep building and improving. Development impact fees don’t provide that.”

Those fees, calibrated carefully through complex economic estimates and political hoops, are more than what most cities do. And yet they are often insufficient.

Cohen claimed that the additional costs needed to fund the city’s smart growth plans outpace the projected fee revenues two to one. Without an influx of public funds, the ledger is empty. “So far,” he said, “there’s no real game plan for it.”

In Chicago, where TIFs were halted for different political reasons, Mayor Emanuel has moved in a new direction. In April, his council officially approved the first municipal infrastructure bank, a pool where private equity invests for the expected returns on public projects.

Observers there are skeptical of its potential, particularly as a substitute for traditional public finance. “The city has a privileged place in the bond market,” Bennett said of the plan. “It’s all pretty mysterious at this point.”

Along the spectrum of value capture policies, at one end sits Henry George’s idea of a single tax on land, regardless of improvements made on it. At the other end are privatization plans, where cities hand over property via long-term leases or, as in Chicago, pay back private investors.

At this end, the deals are often lopsided. And the man who spelled this out for me is one of the biggest private developers in a major American city.

In the privatization model, explained Anthony Pangaro, the private sector sells the deals confidently: “‘We know how to do this, we’re businessmen, we’re efficient.’ There’s another component in any privatization scheme,” he said, “which is profit.”

When that future profit is calculated incorrectly — like Chicago’s parking meter lease, as Emanuel is now painfully learning — cities usually lose out. “You sold the old City Hall and you made a buck,” Pangaro went on. “The only reason that the private sector is willing to do that is that there’s profit involved. You then are paying too much for something you should have been able to buy less expensively.”

Across Arizona, over the past few decades, thousands of private residential groups have popped up and promptly discarded local government. In these homeowner associations, residents eschew property taxes, instead chipping in to pay for utilities. “They’re not value capture,” explained Ingram, “they are cost recovery fees.” Once the housing crash swept through the sand state, hundreds of these associations hiked fees, stopped services or went broke. For Ingram, the lesson is clear.

“We’ve been providing infrastructure through municipalities for 200 years,” he said. “The evidence is that it works pretty well.”

With value capture private funding, public assets remain in public hands.

But getting businesses or developers to pay for street cleaning, in Boston and Bogotá, is relatively easy. Getting them to cut a check for a massive new transit system is not. As Pangaro noted, “you can’t un-build a line.”

Finding outside capital for large-scale public infrastructure has been exceptionally difficult in the U.S. And yet the U.S. may have its first major transit system, funded using the principles of Henry George, in the place where ambition, like all things, is outsized.

Two summers ago, the Dallas Area Rapid Transit (DART), the top provider of transportation for the sprawling metroplex of nearly 7 million, announced severe cuts. It would slice upwards of $50 million from its budget. Projects were ended, staff released, nearly a third of its 20-year transportation plans was shelved. A light-rail, scheduled to be the second to stretch through downtown Dallas, was tabled entirely.

The news arrived as other large-scale projects across the country were also dropped, surrendered or held up in political squabbles. Gas and surface transportation taxes, the usual sources of transit, had fallen woefully short. Statehouses and Congress, clamped down after exiting the recession, refused to give more.

But DART did not give up on its search for funds. In 2010, the North Central Texas Council of Governments, on behalf of DART and other regional entities, turned to the consulting group Gateway Planning to orchestrate a new financing vision. The team cobbled together an extensive financing plan for the Cotton Belt Corridor, a 62-mile passenger rail system that snakes from downtown Fort Worth through its suburbs and those in Dallas, the international airport, a medical center, multiple universities and towns, and into another light-rail service. It would be an immense feat.

“Traditional funding sources simply cannot get the job done in this global economy,” their report reads. The corridor would rely on layers of value capture, primarily TIF and special assessment districts.

It is, however, primarily a public-private partnership. It will break ground, much like Emanuel’s municipal bank, with private investors paying upfront for returns based on the land value increases (this in addition to local public revenue sources). The report projects a total incremental growth of more than $1 billion.

“The developers are happy,” said Scott Polikov, president of Gateway Planning. “They’re not writing checks. This is about increasing the local capacity for property taxes and sales taxes.”

The planners are floating ideas for additional assessment districts, beside or atop the TIFs. But those remain uncertain. Their primary tactic is form-based coding, a planning tool designed to generate stronger tax bases through rezoning.

First, Polikov must thread through 13 different municipalities in the corridor. “Of course, the Cotton Belt does not plow through open land,” as the Dallas Morning News put it. “There is a blizzard of jurisdictions to deal with.” And within each jurisdiction is a patch of varying zones that the rail line would cut through.

That pile of red tape is the least of Polikov’s concerns. He claims to have already rezoned three of the 26 stations along the line. “We don’t have the kinds of wars around growth that other people have,” he said. “That approach to zoning fits well within the free-market environment in Texas.” Adding, “these communities want this.”

“The only reason that the private sector is willing to do that is that there’s profit involved.”

Another financing approach considered for the Corridor is “smartcard” fare technology that would adjust prices flexibly based on demand. The inspiration for that, Polikov said, comes from Hong Kong, where a quasi-public group, the MTR, operates an expansive rail line on a lease from the government. Repeated studies have shown that properties close to the rail line see rapid, undeniable value increases.

Yet, in crowded Hong Kong, around 90 percent of travel is made on transit. In the Dallas-Fort Worth metroplex, several of the 55 light-rail stations DART currently operates reportedly have fewer riders now than when they opened. In the free-market environment of Texas, people like to drive.

Still, Polikov argues that the demand for density is there. The corridor’s biggest obstacle, by his measure, is aligning investors with appropriate returns. For private financiers, investors or developers, this infrastructure model is very novel. It’s “pay before you go,” according to Pangaro. “I’m writing a check at least five years before I would see anything, and probably ten.” This lag, he said, is “the flaw that has to be overcome.”

For the corridor, Polikov is searching for a “different type of investor.” With value capture at its core, the project needs one comfortable with real estate risk.

“There’s just nothing done this way since the time of Rockefeller,” he said. “There’s gotta be a first adopter.”

When Boston first floated the idea for its Silver Line expansion, Frank McCourt lobbied hard for a station on his turf. He even drew elaborate plans for a design equipped with an upside-down pyramid, recalled Vivien Li, president of the Boston Harbor Association. McCourt understood the value the project would bring to his bottom line.

For Boston, where land is scarce, beefing up its mass transit is integral to the city’s economic livelihood. But without a well of financing, the city must pay for it in reverse. “Because we don’t have the funds,” Li said, “the mass transit will have to come after the development. At that point, it will become even more expensive because of the takings.”

Always at hand with the concept of value capture — that government should benefit from the value it adds — is the idea that private owners should be compensated appropriately when public actions reduce their property values. That definition, though, is constantly in legal dispute.

McCourt’s story is telling: To build and expand the Big Dig, city and state government had to temporarily lay claim to parts of his property. What followed was one of the biggest eminent domain cases the city had ever seen.

“If you’re going to tax away benefits,” Ingram explained, “you really need to address compensating people for partial takings,” the legal term for a governmental seizure of portions of private property. “I think it’s a basic fairness point,” he continued. “If you’re going to tax away my gains, you ought to compensate my losses.”

An owner roped into a TIF, or asked to pay an impact fee, could take the policy to court. Complicating the proposals even more is the difficultly of properly assessing the incremental gains in land values. It’s an extremely muddled process. In a recent survey of Latin American officials on value capture, this assessment hardship was named one of the most common hindrances.

But some experts don’t see legal challenges as a major obstacle for value capture policies in the U.S. “Partial takings almost always lose,” explained John Echeverria, a professor at the Vermont Law School. Despite robust protections for property rights, the legal precedent around takings, he said, gives “blinking yellow lights for local governments.”

A bigger hurdle may be politics. The reason the Bay Area is so advanced, procuring more private funds for infrastructure than other cities, is the obvious one.

“I don’t think that anyone who goes into a city like Berkeley or San Francisco is naive about the politics there,” said Stivers. Elsewhere, real estate can wield political power with little organized push back.

And pushing these new forms of land use broadly would require deep cultural change. A couple decades ago, Montgomery County, Md. tried a scheme to spur development that pre-dated the CEPAC in São Paulo. The county rezoned a swath as a conservation region, offering sellable “transfer of development rights” (TDR) in a bid to bring density to another area, the suburb of Silver Spring. It did not go well.

“The county was very good at down-zoning the property,” Ingram explained. “It turned out not to be very good at providing areas where the TDR could be used.”

When Nico Calavita, the inclusionary housing expert, is asked what is holding back value capture policies here, he answers quickly and simply, writing, “They are not part of the planning culture of the U.S.”

In recent years, smart growth planning has steadily taken off. More cities are now aware of the benefits of density, and are putting together zoning changes to unleash it. Without value capture, a gap emerges between the sizable plans laid out and the funds needed to meet them. “The rhetoric on smart growth,” argued Peter Cohen, “is not being matched by the necessary resources to create these communities.”

To fill this gap, he believes value capture principles must be ingrained in city planning. When a planner leaves school, or when a city official arrives in office, they will consider ways to create economic value. Cohen wants to first question they ask to be: Now, how can I capture that value?

Our features are made possible with generous support from The Ford Foundation.

Mark Bergen is a journalist formerly from Chicago and now based in Bangalore, India. He writes the Econometro blog for Forbes.com and has covered politics and policy for GOOD, The Atlantic Cities, Tablet Magazine, Religion Dispatches and the Chicago Reader.

Tim Pacific is an award-winning graphic design student entering his senior year at Rutgers University in Camden. In addition to his schoolwork, Tim is an active freelance illustrator. His work can be seen in AIGA Philadelphia’s SPACE, which features a recently completed series of hand-lettered postcards. Among his design philosophies, Tim believes strongly that concept comes first and you should absolutely judge a book by its cover design.

Next City is a nonprofit news organization that believes journalists have the power to amplify solutions and spread workable ideas from one city to the next city. Our mission is to inspire greater economic, environmental, and social justice in cities.

Learn more about us →

20th Anniversary Solutions of the Year magazine