The first time Andreanecia Morris remembers learning about the Community Reinvestment Act was at the Housing Authority of New Orleans, where she started her career in the mid-1990s. During her time there, the authority created its Section 8 Homeownership program, which allows families with rental assistance vouchers to convert them into mortgage assistance payments instead. But the housing authority still needed to convince banks to create a mortgage product that would be compatible with the Section 8 Homeownership program. It was the Community Reinvestment Act that brought banks to the table.

“They would get CRA credit for this,” Morris says. “That’s the kind of responsiveness [from banks] that you needed, the thoughtfulness in saying, ‘Listen, this isn’t a risk, it is to [our] benefit and [we’re] making a good investment’ — these are loans, not a gift to the homeowners.”

The CRA, a decades-old law meant to ensure banks meet the credit needs of the communities they serve, is in need of an update — both banks and community organizers agree. While 98 percent of banks get a passing grade on their CRA exams, it’s not always clear that their investments are actually benefiting locals. Yet today, there are federal regulators who want to gut the CRA — an effort CRA proponents have called “an attack on communities of color.”

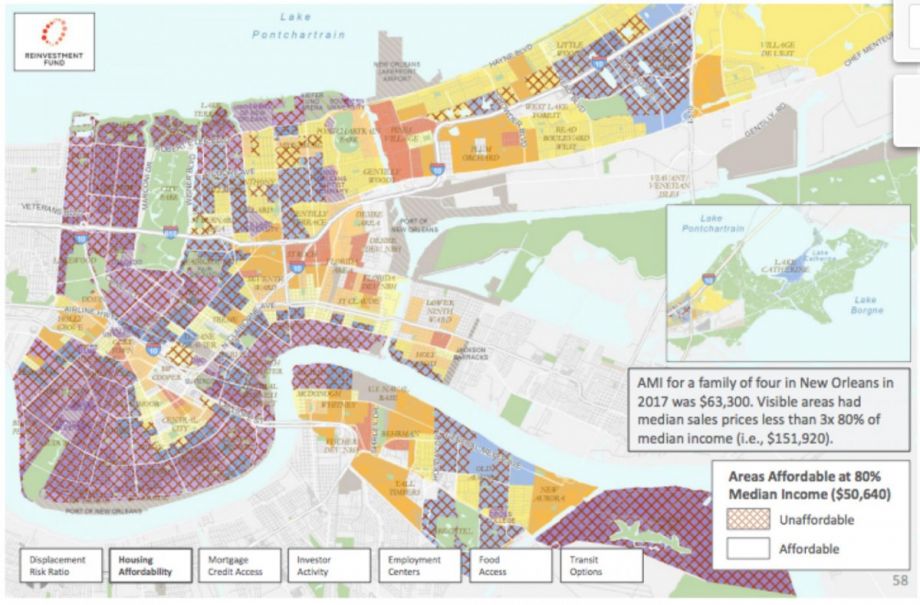

But Morris and the coalition of partners she now leads, known as HousingNOLA, are hoping to make the CRA work better for low- and moderate-income communities as well as for banks. HousingNOLA recently published its first ever Community Development Finance Plan, providing estimates of how much investment is necessary to serve renters and homeowners in danger of being displaced.

“We’re going to make it really easy for banks to talk about the buckets of investments that are necessary and get to the point where we can say [to banks and regulators], ‘If your investments don’t hit any of these thresholds … you have not met this community’s needs,’” Morris says.

The impetus for the plan dates to 2016, when HousingNOLA issued its first report card on the progress of its 10-year Strategy and Implementation Plan for a More Equitable New Orleans.

“We said, ‘We’ve got to make sure the public partners buckle down, but we cannot ignore the private partners — this is not a problem that government money can fix on its own,’” Morris says.

Morris and other coalition partners had been witness to what happens when the private sector isn’t held accountable. In the ten years after Hurricane Katrina, she explains, the city and private sector partners had managed to create 88,000 units of subsidized affordable housing. Some critics claimed that was too much, but Morris and others saw it differently. Long-time residents of New Orleans, the people whose music and food make the city the tourist draw that it is, were still being displaced.

Even with the 88,000 new subsidized units, “we still found ourselves in the worst affordability crisis the city’s ever seen — because all of that was done without a cogent data-driven, community-rooted plan,” Morris says. “It just happened.”

Worse yet, according to Morris, banks were getting CRA credit for making investments in low-income neighborhoods to build housing that wasn’t affordable for low-income residents, or support businesses that didn’t serve existing communities. “Making an investment in a low-income neighborhood and making an investment in a luxury building that is just a force for gentrification is not, in my opinion, adequate,” Morris says. “But it will count toward CRA if it’s not properly contextualized.”

The CRA was the last big piece of civil rights legislation, passed in 1977, thanks in no small part to Gail Cincotta and other community organizers from the West Side of Chicago. Even after the Fair Housing Act of 1968, it was widely understood that banks were still redlining low-income areas, especially in cities, where such neighborhoods were predominantly home to people of color (not to mention many white households in rural areas). Earlier work like the Kerner Report had made clear the consequences of that neglect.

Fast-forward to today, and banks have become more than willing to tell regulators about investments they make in low-income areas. But the law still doesn’t require that banks show how those investments benefit residents of those areas. As others have shown, bank loans to acquire or renovate buildings in low-income areas can sometimes be made specifically to displace those residents and businesses.

What might seem like the CRA’s biggest flaw is also its saving grace — it’s actually very vague. It says regulated financial institutions have a “continuing and affirmative obligation to help meet the credit needs of the local communities in which they are chartered,” but it doesn’t specify a process for determining those credit needs. The law empowered federal regulators to do that, and over the decades that has been an evolving process that both banks and community organizers have characterized as inefficient and inadequate.

If a bank does fall short, regulators can deny proposed mergers or place growth restrictions on banks. The National Community Reinvestment Coalition and its grassroots partners have — by mobilizing to offer comments on CRA examinations or bank mergers — negotiated more than $82 billion in lending commitments from banks to low- and moderate-income areas over the past three years.

One of the chief complaints from banks about the CRA exam is that the process of determining a community’s credit needs can be inconsistent and unpredictable from one CRA exam to the next, usually three to five years later.

Morris frames HousingNOLA’s Community Development Finance Plan as a way for regulators and banks to have more clarity — that if a bank’s activities met the needs outlined in the plan, it should definitely get CRA credit for those activities.

“We are trying to take advantage of the rules as they are today, and [ensure] that they are consistently enforced,” Morris says. “We do have the opportunity to be heard, [and] our members, our resident leaders, understand this.”

Despite the shortcomings of current regulations for determining community needs, banks’ CRA-eligible community development lending continues to increase, reaching $96 billion in 2017, according to the Federal Financial Institutions Examination Council — that’s up from $87 billion in 2015 and $65 billion in 2013. Documents like HousingNOLA’s Community Development Finance Plan can affect where those dollars end up.

There is already some precedent for plans like these. While not every plan has the same level of community engagement or community leadership, it’s an accepted practice for banks to seek out master plans, comprehensive plans, neighborhood plans and other planning documents to identify or justify investments made for CRA credit. Banks may not even tell planning departments that they’re using their documents as part of their CRA compliance process. “We just pull [the plans off the internet],” one CRA officer told me at the NCRC gathering earlier this year.

Morris would like regulators to go even further — to have regulators give banks CRA credit only for activities that meet the specific needs outlined in planning documents made with community leadership.

“We’re joining the national chorus of voices saying not only do you need to strengthen [the CRA], you need to make it more responsive to community,” she says.

So far, they’ve gotten a mostly positive response from banks with business interests in New Orleans. Even with the recent policy victory of New Orleans’ new inclusionary zoning regulations, Morris and HousingNOLA aren’t expecting that policy alone to net all 33,000 new affordable housing units they estimate the city needs. It remains to be seen whether developers will get access to enough capital and at the right interest rates to hit that target.

“Some of the banks have responded really well, and it doesn’t mean they’re on the ground where we need them to be, but they are open to the honest reflection and trying to work with us,” Morris says. “Some of them meanwhile are like, ‘Wait, what are you talking about?’”

The HousingNOLA Community Development Finance Plan includes the formation of a “Lenders Roundtable,” described as “a collection of financial institutions, real estate experts, government agencies, developers and advocates that are committed to securing financial investments necessary to address the affordability crisis.”

The Lenders Roundtable includes representatives from the five largest banks by deposit market share in the New Orleans metropolitan area: Capital One and Hancock Whitney — which combined control $16 billion out of $34 billion in total metropolitan area deposits — as well as JPMorgan Chase, Regions Bank and Iberia Bank.

“We’ve gotten a good response rate from the banks we need to participate in the conversation — the devil is going to be in the details of their investment strategies,” Morris says. “We also have some smaller banks that need to be wrangled. It’s not just the big boys.”

This article is part of The Bottom Line, a series exploring scalable solutions for problems related to affordability, inclusive economic growth and access to capital. Click here to subscribe to our Bottom Line newsletter.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)