‘Tis the season for Opportunity Zone investing. The new tax incentive to invest in economically distressed areas was already drawing significant interest before Oct. 19, the day when the Internal Revenue Service (IRS) proposed key guidelines that many were waiting upon to begin making their cash available for investment in designated Opportunity Zones. The guidelines provided important clarity on a number of questions that were still preventing a large number of investors from making their cash available for Opportunity Zones.

A number of Opportunity Funds — vehicles for aggregating the funds to make multiple Opportunity Zone investments — are already forming. Novogradac & Co., an accounting firm that specializes in community development finance, published a directory of 21 Opportunity Funds, with stated goals to raise as much as $4.8 billion in capital under the new tax incentive. The National Council of State Housing Agencies also published a directory of Opportunity Funds, with some overlap between the two. Under the new law, it’s also possible to create single-investment Opportunity Funds for investing in just one eligible business or property.

Treasury Secretary Steven Mnuchin has said that he anticipates as much as $100 billion in investment through the Opportunity Zones tax incentive. As Next City has reported recently, many in fast-growing cities such as Austin, Texas, are concerned that the flood of capital could exacerbate existing gentrification challenges, while others in places such as Alabama are eager to connect investors to projects in places that haven’t had much access to community development capital before.

Federal records show four meetings hosted at the Office of Information and Regulatory Affairs to discuss the proposed guidelines before their release. Attendees included representatives from the Department of the Treasury, major accounting firms, lobbyists for the logistics industry, departments of economic development or commerce from six states, Economic Innovation Group (the think thank that hatched the Opportunity Zones tax incentive) and venture capitalist Ross Baird.

If you are still getting informed on Opportunity Zones, you’re far from alone. The program has only been around since the passage of the Tax Cuts and Jobs Act at the end of 2017. The program offers tax breaks on capital gains income for investing in designated Opportunity Zones across the country.

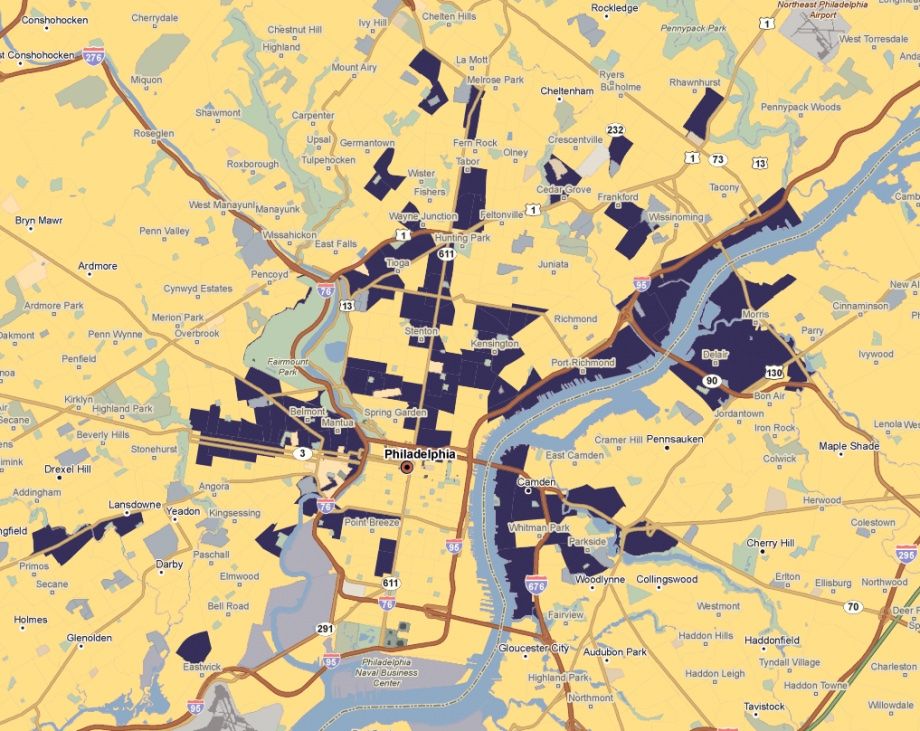

The new law gave states, specifically governor’s offices, the responsibility to select Opportunity Zones from among eligible census tracts. To be considered eligible, census tracts had to have a poverty rate of at least 20 percent or a median family income not exceeding 80 percent of median family income for the metropolitan area or statewide median, whichever is higher. States could select up to 25 percent of eligible census tracts, and up to five percent of their selections could also be census tracts that did not meet qualifications themselves but were adjacent to an eligible census tract. Based on those parameters, out of 42,176 possible census tracts, all 50 states, five territories and the District of Columbia chose 8,762 census tracts to receive designation as Opportunity Zones.

The designation process intentionally differed from the EB-5 Immigrant Investor program, which allows foreign investors to “buy” permanent U.S. residency by making an investment in a project located in a distressed area. Under the EB-5 program, developers can gerrymander census tracts together to create an “area” that meets the unemployment threshold of the program, with the project receiving the investment located far from areas of actual high unemployment. That won’t be possible under this program.

Some 35 million people live in designated Opportunity Zones, with a majority being people of color, according to an analysis by the nonpartisan Urban Institute. The same researchers also created a ranking of census tracts based on existing investment trends, which revealed that many selected Opportunity Zones are already receiving a significant amount of outside investment. In selected metropolitan areas, they also found, a large proportion of selected Opportunity Zones are already experiencing demographic shifts toward more highly educated, higher-income households.

Here’s how the tax incentive works: If I have a million dollars in capital gains income, from the sale of stock or real estate or other assets (including works of art), I can temporarily defer federal tax payments on that capital gains income by investing the million dollars directly into an eligible business located in an Opportunity Zone or into an Opportunity Fund, which must invest at least 90 percent of its assets into eligible businesses located in Opportunity Zones. Eligible businesses include real estate projects (excluding golf courses, country clubs, massage parlors, hot tub or suntan facilities, race tracks, gambling establishments or liquor stores). If I leave the million dollars in this investment for five years, I get a ten percent reduction in my original capital gains taxable income; if I leave it for seven years, I get a 15 percent reduction; in other words, I’d be taxed on $850,000 of capital gains income instead of the original one million. Bonus: if I leave the funds invested for at least ten years, any new capital gains income from that investment are tax-free at the federal level.

One of the key questions addressed in the new IRS guidelines pertains to the timeline of raising capital versus actual investment in eligible projects or businesses. While investors want the tax benefits right away, real estate projects can take years to aggregate necessary capital, especially if they are projects with an intentional plan to benefit communities. Under the new guidelines, Opportunity Funds have 31 months from receiving capital from investors before they must invest the capital into an actual project — provided that they have a plan to do so within six months of receiving the capital. That means investors can have the confidence to invest in Opportunity Funds with a pipeline of projects that might take longer to come to fruition for the sake of community benefit.

Another key question concerned the law’s requirement that businesses receiving Opportunity Zone investment must conduct “substantially all” of its business inside an Opportunity Zone — as a safeguard against businesses registering an address inside an Opportunity Zone for the purposes of raising capital without actually hiring anyone or serving anyone inside that Zone. Under the final guidelines, at least 50 percent of the gross income of an eligible business must come from “the active conduct of a trade or business in the qualified Opportunity Zone.” Some advocates were hoping for a higher percentage, but others feared that might discourage investors from taking advantage of the program.

The IRS also created a “70-30 rule,” permitting up to 30 percent of an eligible business’ property to be located outside a designated Opportunity Zone. So if a local restaurant chain has five locations, for example, at least four of them must be inside an Opportunity Zone.

On other suggested safeguards, the IRS has so far been mute or is leaning more toward being friendly to investors instead of the 35 million Opportunity Zone residents. Despite calls from advocates to do so, there are no guidelines for eligible businesses to hire residents who live in the Opportunity Zones where they are operating, nor are there requirements that any housing units created with Opportunity Zone capital be affordable for existing residents of Opportunity Zones. The IRS also released a draft version of the required form to “self-certify” as an Opportunity Fund. The form is one page long, two if the fund is “out of compliance,” and the only measure of compliance is the percentage of the fund’s assets located inside a designated Opportunity Zone. Opportunity Funds must pay a nominal fee — based on how much the fund is below the 90 percent threshold — for each month in the previous tax year they are not in compliance.

With so few “guard rails” at the federal level, some are looking to states or municipalities to create measures for protecting Opportunity Zone residents from displacement, or at least incentives to encourage more responsible behavior on the part of Opportunity Funds.

“We believe the state, in designating these zones, has a responsibility to protect the communities that are already there and make sure they benefit from these zones,” Paulina Gonzalez, executive director of the California Reinvestment Coalition, told Next City earlier this year.

Oscar is Next City's senior economic justice correspondent. He previously served as Next City’s editor from 2018-2019, and was a Next City Equitable Cities Fellow from 2015-2016. Since 2011, Oscar has covered community development finance, community banking, impact investing, economic development, housing and more for media outlets such as Shelterforce, B Magazine, Impact Alpha and Fast Company.

Follow Oscar .(JavaScript must be enabled to view this email address)