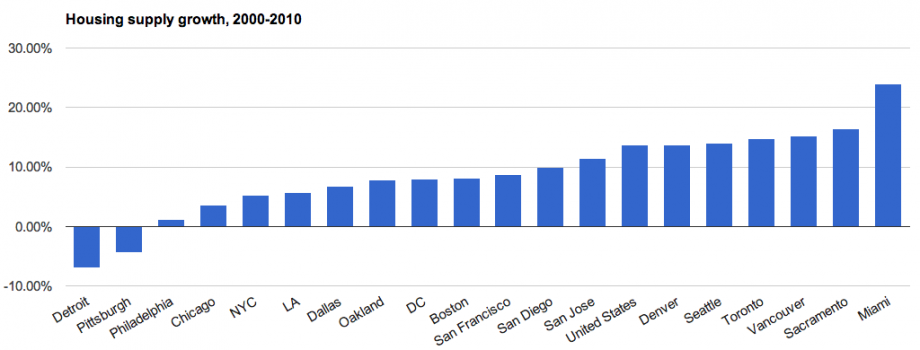

A few weeks ago I compiled a spreadsheet of housing unit counts for various U.S. cities, plus Toronto and Vancouver, over the past few decades. Presented above is a chart of housing growth in these cities according to the 2000 and 2010 censuses. I chose the selection somewhat randomly, but tried to encompass most major North American cities that did not annex significant quantities of land — which would skew the statistics, but ruled out many fast-growing areas of the Sun Belt. While the data only represents cities proper, all of the given cities are fairly urban, with at least 30 percent of the housing stock in multi-unit rather than single-family structures in 2010 (with the exception of Detroit).

One detail sticks out: Many of the largest and most desirable cities have struggled mightily to keep building as much as the country as a whole, which is presented as a baseline. There appears to be little correlation between growth and demand aside from in Detroit and Pittsburgh, cities that lost housing units in the first decade of the new millennium. Denver and Miami are by no means undesirable cities, for example, but it seems unlikely that they’re more in demand than New York and San Francisco.

There are a few other notable points, not least of which is the incredible building boom in Miami. The city had 24 percent more houses and apartments in 2010 than it did in 2000. That means more than 35,000 new units. Of those, the vast majority were in fairly large buildings with at least 50 units. This is consistent with the towers that sprouted like weeds in downtown Miami and neighborhoods like Brickell. Given that Miami development is back with a vengeance, we may see huge growth in this decade as well.

Another obvious takeaway is that Canada’s two largest cities are booming (in Canada, the timeline runs between 2001 and 2011). Both Vancouver and Toronto posted Houston-like housing production numbers, even without Houston’s annexation. Since these Canadian cities are largely built out, it stands to reason that the vast majority of the new construction was infill, consistent with the stereotype of Vancouver and Toronto as besieged by high-rise condo developers. (Canada has almost no new rental construction, likely due to its tax policy. Condo units are instead rented out on an individual basis.)

Seattle and Denver also did very well in housing production, besting the national average. In both cities, the vast majority of new units were in structures other than single-family detached homes. The largest category of construction in Seattle comprised buildings with 50 units or more, though single-family attached units — rowhomes and semi-attached homes — nearly doubled in quantity from a base of about 6,000. Denver saw a bit more single-family detached home building: Around a quarter of its added units came in this type, with the rest spread throughout denser structures. The plurality came in the 50-plus unit category.

In Sacramento, on the other hand, the vast majority of new units were single-family detached houses, in line with stereotypes about the city. But as Seattle, Denver, Miami and the two Canadian cities show, healthy growth in a North American city’s housing stock need not come from sprawling subdivisions.

Beyond these cities, there weren’t too many surprises. San Francisco actually grew its housing stock faster than New York. Dallas didn’t grow very fast at all, and Oakland grew at a faster rate than Los Angeles. The underlying data, which includes numbers for 1990 in many cities, is available in this somewhat messy spreadsheet.

The Works is made possible with the support of the Surdna Foundation.

Stephen J. Smith is a reporter based in New York. He has written about transportation, infrastructure and real estate for a variety of publications including New York Yimby, where he is currently an editor, Next City, City Lab and the New York Observer.

{kind=link}