Are You A Vanguard? Applications Now Open

This is your first of three free stories this month. Become a free or sustaining member to read unlimited articles, webinars and ebooks.

Become A MemberWhen Robert C. Blackburn talks about the future of the Port of Philadelphia, he gets excited. Just ask about the plan to transform 120 acres of rubble-strewn lots, rusting cranes and dead-end railroad tracks in South Philadelphia into a gleaming new container terminal, and prepare to sit tight. He’s got a lot to say.

Blackburn, senior deputy executive director of the Philadelphia Regional Port Authority (PRPA), speaks in a rumbling Philly accent. His sizable frame nearly bursts out of his neatly pressed suit jacket as he jabs at satellite images of the property near Front Street and Pattison Avenue, land that his agency has assembled for the proposed facilities, called Southport. His gruff demeanor makes Blackburn seem like he’d be more comfortable at the controls of a container crane than in the stuffy boardroom we inhabit with two other port authority executives. But it’s logistics and the speculative economics of shipping traffic that motivate him.

Blackburn has good reason to be excited. If successful, Southport will be, in 2013, the first major expansion project the Port of Philadelphia has seen in decades. The partially state-funded expansion his organization is spearheading will, he says, translate into $250 to $450 million of private investment and 6,000 new jobs, tripling the nearly 2,000 current employees at the port. These are figures that resonate in many struggling, older East Coast anchorages that have seen cities like Long Beach and Oakland, Calif. soak up explosive trade from China for reasons that one need only glance at a map to understand.

Jobs. Money. What’s not to like? Ports are unquestionably important economic drivers, one of few that have not wholly evaporated in some coastal Rust Belt cities. Yet push past the enthusiasm of boosters like Blackburn, and complex uncertainties begin to emerge. At the crux of the debate is a simple question: Is a big-ticket port expansion the right way to create jobs for 21st-century Philadelphia?

Mayor Michael Nutter and other local leaders have increasingly positioned Philadelphia as an “incubator of innovation” at the forefront of the country’s post-industrial “new economy. ” In a recent op-ed co-authored with Rep. Chaka Fattah, Nutter made the case for public investments that help “transform Philadelphia and cities across America as they move from 20th-century manufacturing-based economies into global, innovation-based ones.”

Pier 98, a currently abandoned port facility to the north of the Packer Terminal. In 2010, the PRPA had slated the pier for use as part of an expanded Hyundai loading area.

As shifts in the global economy transform the way cities do business, does this port expansion fit into that broader economic development strategy? Or is demand for the project driven more by the desires of well-connected players that benefit from infrastructure spending? Is there strong evidence that these investments will pay off? Or are projections inflated, like so many stadium and convention center projects that promise more public benefit than they deliver?

The City of Philadelphia, for instance, has already sunk billions of dollars into demolishing and upgrading a convention center deemed obsolete in the ’80s, only to see the new center compete against the myriad other cities that made similar investments while watching the market contract as companies moved conversations online. Philadelphia’s massive stadium complex pulls in many fans, but pays little in local taxes. More pressingly, it has failed to spin off development to the crumbling industrial neighborhood it was supposed to reinvent.

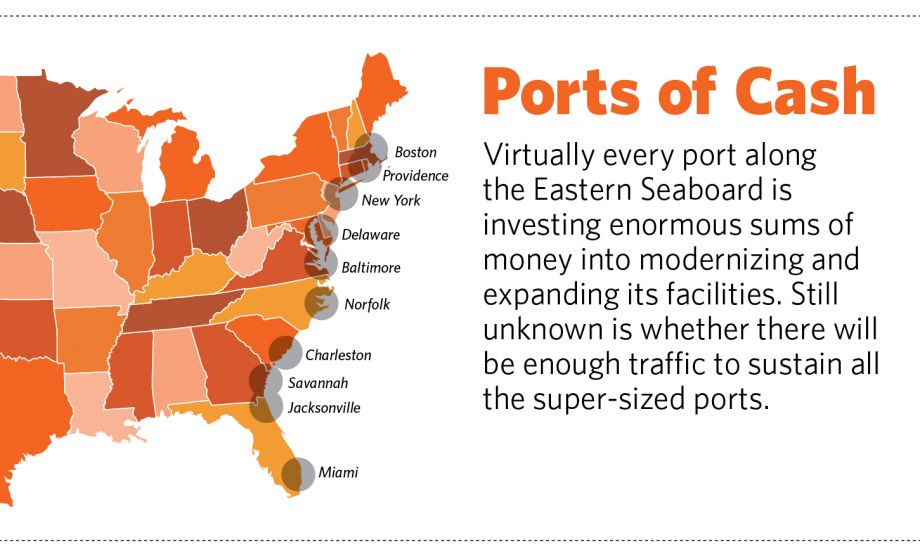

Like the convention center fad, a project like Southport is not an investment unique to Philadelphia. It is one of nearly 30 similar port expansion projects along the East Coast, all of which are large, capital-intensive projects that rely on significant government subsidies. Public investment in port facilities alone is expected to total $14.4 billion in 2012, while industry associations, like the American Society of Civil Engineers, indicate that port authorities are seeking a further $15.8 billion through additional private and public partnerships. The expansion of transportation infrastructure — new rail and highway projects to better connect ports — is also projected to run into the billions of dollars.

On the East Coast, virtually all of these dollars are being spent with the presumption that a project to expand the Panama Canal, due to be completed by 2015, will bring bigger ships and therefore more Asian cargo directly to the East Coast. The trouble, analysts say, is that no one really knows how much new traffic the widened Canal will actually produce, particularly for older shipping lanes that suffer from natural disadvantages, like shallow waterways and geographic separation from the open sea.

Like the convention center fad, a project like Southport is not an investment unique to Philadelphia. It is one of nearly 30 similar port expansion projects along the East Coast.

“[The Panama Canal] raises a lot of very significant questions,” says Adie Tomer, senior research associate at the Brookings Institute’s Metropolitan Policy Program. “A lot of municipalities across the country have made some pretty significant investment decisions that we’re not certain are backed by ample quantitative metrics.”

Even more problematic is that the simultaneous expansion of East Coast ports, often partially subsidized by state and federal dollars, is not part of a larger cohesive plan to manage growth, but more a scramble to be the port that catches the lion’s share of a possibly elusive new source of traffic. This raises the threat of overbuilding and redundant, underused facilities.

Analysts like Tomer see a potentially wasteful game of brinksmanship at play.

“The question is, what is the end goal here?” says Tomer. “Is it a winner-take-all race where one port is going to ‘beat’ the other? Or is there an opportunity to pool resources and work together?”

Blackburn’s Port of Philadelphia is no exception. In fact, its unique set of challenges — being situated eight hours upriver from the sea, along a channel too shallow to handle modern super freighters, while competing with dozens of other facilities in three different states — make it a poster boy for the problems and uncertainties facing many East Coast seaports eyeing the Canal as a panacea.

Like many older East Coast cities, Philadelphia was, for over three centuries, defined by its role as a center of maritime trade. Up until the latter half of the 20th century, its streets were packed with visiting sailors and naval officers, while nearly 100,000 longshoreman and shipwrights labored in the mammoth Navy Yard and on bustling piers that curled along a booming riverfront. The prosperity of the seaport was fueled in large part by the manufactured goods that earned Philadelphia its reputation as “The Workshop of the World.”

But all that started to change in 1956 with the advent of containerized cargo. The now-iconic metal boxes could be lifted directly out of a ship and onto a freight train or big rig, facilitating faster and more efficient shipping at the expense of the laborers who used to manually unload boxes of “breakbulk” cargo. In addition to shedding jobs, the transition also brought the need for immense new cranes and rendered the city’s expansive but tightly packed “finger pier” system increasingly obsolete, as ever-larger freighters took advantage of modular cargo. Newer port facilities were built in Philadelphia, with state assistance, to handle “modern” cargo.

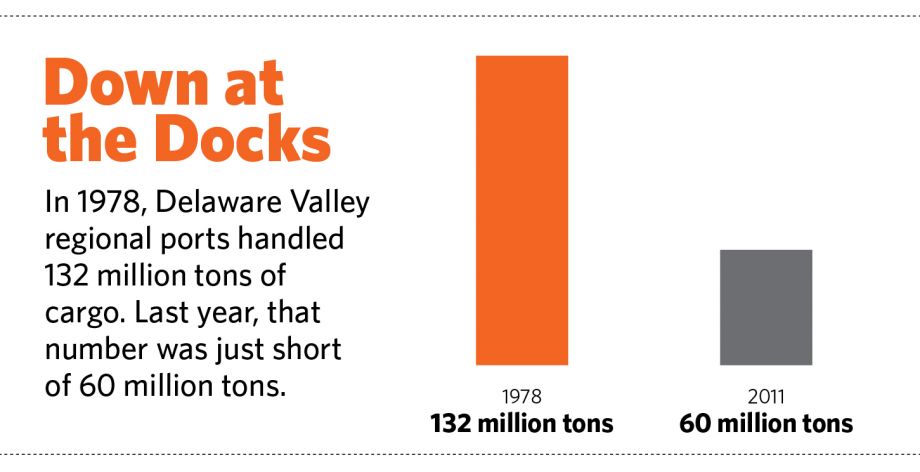

But the expected container traffic never fully materialized. While the smaller, older piers started collapsing into the river from disuse, the container trade at the new terminals remained, at best, inconsistent. In addition to the global container market’s sensitivity to economic boom and bust cycles, history has seen the majority of container traffic end up at a handful of “strategic ports,” like New York, that have quick and easy access to the open ocean — something that Philadelphia simply does not possess. Time is crucial for large container ships; port officials noted that each extra minute at sea adds a dollar to the cost of moving a given container.

Additionally, speculation that trade would shift back to the East Coast has been consistently dashed by East Asia’s continual manufacturing dominance. Painfully, Philadelphia’s own decline as an industrial center means many freighters must leave empty-handed, further driving up shipping costs.

Today, tens of thousands of jobs have been lost through declining traffic and automation. Exactly how many people work on the waterfront is a point of controversy because public investment is often tied to how large, and therefore important, is the port in question. A 2008 Economy League report found that port facilities in Philadelphia directly employed 1,945 people, supporting an additional 2,336 indirect jobs through maritime industry demands. Regionally, ports employ, directly or indirectly, 12,121 people, 4,216 of whom reside in Philadelphia, according to the Economy League.

It’s a figure disputed by Philly’s port authority. Nick Walsh, director of strategic planning and development at the PRPA, says that the Economy League’s methodology led to inaccurate results. Walsh asserts that, according to the authority’s in-house statistics, 5,276 people are directly and indirectly employed in Philadelphia alone, part of an estimated 47,320 port workers in the tri-state region. Walsh says he could not publically release methodology on how these figures were reached. Steven Wray, executive director of the Economy League, says he cannot account for the differing figures, but that his organization “showed its work,” referring to the publically available methodology used in their report.

Backhoes dig out the site for a new Marriott Courtyard Hotel in the Philadelphia Navy Yard, near a soon-to-be-completed headquarters for Iroko Pharmaceuticals.

Whatever the true number, anemic traffic levels on the Delaware River speak for themselves. While a 2011 American Association of Port Authorities report ranked Philadelphia as the nation’s seventh-largest port in terms of trade tonnage, most analysts recognize that the city’s large oil refinery complexes, and their associated seaborne petroleum trade, buoy this number. Sunoco and other oil companies account for fully 65 percent of Philadelphia’s annual tonnage, but the quick-and-easy processing of petroleum tankers makes up only 10 percent of port employment. There are simply more jobs in container processing, an area where the U.S.’s fifth-largest city is ranked 19th nationally, behind Anchorage, Alaska. The port authority now markets its lack of congestion as a strength — shippers might encounter lengthy wait times at busier ports.

Philadelphia is certainly not alone in struggling to keep up with modern demands, as seaports from Miami to Savannah to Baltimore have raced to adapt to rapidly changing trends in shipping. But even as public and private entities continue a kind of arms race to win coveted cargo traffic, the global economy continues to shift. These changes have challenged long-held beliefs in the regional value derived from hosting a port, and a growing number of economists say that, in some cases, investments in the local economy could be a more effective use of money than focusing on the import and movements of products made elsewhere.

“These kind of investments really raise questions about how much it matters today to have goods directly enter and leave through water-based transportation from these particular metropolitan areas,” Tomer says. “Is Philadelphia’s future based on the ports? Or is Philadelphia frankly better positioned to use these kind of investments to help other places in the region?”

But local advocates say that the thousands of good-paying jobs on the waterfront are too important not to bet on. “The number-one reason to [expand] is to protect the business we have,” says Dennis Rochford, president of the Maritime Exchange for the Delaware River and Bay, an organization that lobbies for regional port funding. Rochford says that Philadelphia can stay competitive through channel deepening and by capitalizing on its strengths, like its transit connections and proximity to millions of residents in the Northeastern U.S. “Philadelphia has proximity to a large consumer market,” he says, “and there are three Class 1 railroads coming into the port, and I believe we’re the only port on the East Coast that can say that.”

The Philadelphia Regional Port Authority itself is, in many ways, a last-ditch effort to engineer a comeback on the Philly waterfront. Created in 1989, the $2.5 million-a-year state agency came about as a means to unify and reimagine port facilities after disastrous freight declines in the 1980s. Their mandate was a big one: Figure out a new way forward for the flailing industry. Southport was supposed to be the answer.

Blackburn acknowledges that it’s been tough getting the project off the ground. The regional authority’s role has been mostly to channel public money, about $30 million so far, into land assembly, site prep and infrastructure improvements — like soliciting the city to build new truck only highway ramps — to make the land more attractive. The PRPA will then partner with the private shipping firm Delaware River Stevedores, Inc. to actually build the new facilities themselves.

The end result will largely depend on the needs of the firm, making Southport partially conjectural despite the agency’s grand vision of a new container terminal. Adding to complications is the fact that, while container traffic is slowly increasing, PRPA’s other terminals are “not at full capacity,” Blackburn says.

“When we were marketing the facility we planned it to be most likely a container terminal,” Blackburn says. “Now, until it’s built you never really know… but I can’t say with 100 percent certainty that it will just be for containers.” The authority, he says, has also explored using the land for auto loading and distribution centers.

The port authority now markets its lack of congestion as a strength — shippers might encounter lengthy wait times at busier ports.

The idea that Panama will fuel growth locally is largely based on an assumption that the Port of New York and New Jersey will become congested by its own surge of traffic, and that some will overflow and reroute to Philly. The date for when this will supposedly happen has already been kicked back due to the flagging economy.

“It might not happen overnight,” Blackburn says. “Before the recession we saw New York maxing out at 2016, so we’re just seeing that pushed back. I’d like to think we’re recovering now, but I’m no economist.”

The Port Authority of New York and New Jersey is embarking on its own multibillion-dollar project to dredge the Hudson River and raise the Bayonne Bridge, seeking to dominate post-expansion traffic. Officials from that authority declined to comment on Philadelphia’s expectations of traffic spillover from New York.

Skeptics like Tomer say that any increase is not going be immediately apparent. “There isn’t going to be a moment when they open the new Canal and you’ll see hundreds of freighters lining up for East Coast ports,” Tomer says. “It’s not going to be as simple as snapping your finger.”

Ongoing research already indicates that far fewer U.S. markets will be affected by the Panama Canal project than is widely assumed, and that the largest growth opportunities are in areas distant from Philadelphia, primarily Appalachia and areas directly west of it. Compared to the existing markets in major ports such as Chicago, New York and LA, these markets are small.

If you ask anyone at the port to name the biggest hurdle preventing Philadelphia from competing with its larger cousins, the answer is practically automatic: The lengthy and shallow Delaware River shipping channel. Ironically, the multi-decade quest to solve this problem by artificially deepening the river through dredging — and the inadequate final product — highlights what may arguably be an even deadlier problem for many ports like Philadelphia: regional infighting.

Over the course of the last 14 years, Delaware dredging has progressed in spurts, largely due to political jockeying. In 1998, Pennsylvania began seriously pushing to have the Army Corps of Engineers initiate a dredging project that would deepen the river’s shipping channel from 40 feet, its depth since World War II, to 45 feet, which was more in line with the drafts of modern sailing vessels at the time. Final costs have been estimated at around $255 million.

Although the project would clearly have benefitted port facilities on both sides of the river, key political actors in the region, particularly New Jersey Gov. Chris Christie, strongly opposed deepening the Delaware. Environmentalist groups like the Clean Air Council blasted the project as being economically “unnecessary” and ecologically destructive, as it would stir up pollutants trapped in the riverbed.

Keystone state critics called the obstruction an attempt to play favorites; Christie had silently endorsed an ongoing, near-identical $2.5 billion plan to deepen New York Harbor to 50 feet. The State of Delaware briefly joined New Jersey in a lawsuit aimed at scuttling the Delaware River project all together.

Pennsylvania Gov. Tom Corbett was able to hammer through a deal to complete the project earlier this year, but now state taxpayers will pick up nearly $40 million in dredging costs that were supposed to be shared with New Jersey and Delaware, according to the Army Corps of Engineers. While completion of the project, in 2017, now seems certain, the lengthy battle inflated costs and exacerbated an already acrimonious working relationship between Pennsylvania and New Jersey. This was embodied by Pennsylvania State Rep. Pat Meehan’s comment, at the press conference inaugurating the final phase of the project, that without the dredging jobs would “go to guys wearing Giants and Redskins jerseys, and that just doesn’t seem right.”

Cranes from the existing Packer Avenue Marine Terminal loom over a vacant piece of the Navy Yard that may someday hold the Southport. If completed, Southport will be Philadelphia’s first new container terminal in decades.

Furthermore, while dissipating worries about the dredging project’s completion have put Southport on firmer footing, the delays and political blockade have left Philadelphia, and the rest of the Delaware Valley, with a new channel that is now five feet short of the new 50-foot industry standard. This puts much of the sought-after, post-Canal expansion traffic tantalizingly out of reach, while still compromising the Delaware’s water quality and marine ecosystems.

While macro-level competition between New Jersey’s northern port and Philadelphia has resulted in unbalanced cost sharing and a channel that’s still too shallow, the river’s length leaves ample room for micro-level local rivalry, which can be just as bitter. Between Pennsylvania, New Jersey and Delaware, there are approximately 40 separate port facilities along the river, a dozen of which are in Philadelphia itself.

The different ports aren’t quite friendly competitors. In addition to Southport, authorities in Glassboro, N.J. and Wilmington, Del. have each launched their own competing expansion plans. In the case of Wilmington, the state-owned port is currently accepting bids from private terminal operators to partner in a $500 million container expansion project that is peculiarly similar to Southport.

The projects are being planned independently of one another and seem to risk making each other redundant as they compete for the same stream of freight traffic.

If Blackburn is worried, he doesn’t show it. “Now with each of the three states each trying to develop new terminals, there’s an idea that there could be redundancy moving forward, and there very well may be,” he says. “But, I think it will be a long time before each [of the] three states have all three facilities operating at capacity. We wish them luck, but we think we have a competitive advantage.”

Others say these costly public investments deserve more critical attention and that the various players must work together if they want to survive in an increasingly globalized, regionalized and competitive landscape. “That can be done through certain actors, an agency who doesn’t necessarily have vested interests in any one of the places over another,” Tomer says. “If anything, they should be interested in the entire area being successful.”

The Delaware Valley Regional Planning Commission (DVRPC) is one agency that could fill this role. The Commission acts as a non-biased planning agency on that operates in an advisory capacity for the entire tri-state region, weighing in on everything from highways and public transportation systems to air and seaports. But while the federal agency has the mandate to advise entities in the region, it often sits back and watches as marine projects move forward with little outside guidance.

Ted Dahlburg, manager of freight planning at the DVRPC, says that while his organization “kept abreast” of port issues, they did not weigh in with a regional perspective. “Ultimately, land use decisions are still made at the local level,” he says. “We have no authority.”

The DVRPC may have administrative or functional limitations over how much they can affect port development in the region. But if they are not guiding the larger process, who is?

Another means of bolstering cooperation, used in places like New York and New Jersey, is creating a combined port authority that spans multiple states. The idea conjures bad memories in the Delaware Valley.

Employees at the Urban Outfitters corporate headquarters. This Fortune 1000 company is based in the city’s bustling former Navy Yard, now a tax-free business campus immediately to the west of the proposed Southport site.

In 1993, as legislators recognized that a lack of cooperation was jeopardizing federal funding for port infrastructure, a bi-state attempt was made to create a unified port of Philadelphia and Camden.

Blackburn remembers the attempt, which he calls “fatally flawed.” He says that the political structure of the combined agency favored New Jersey interests, since it allowed the state governor to hold “veto power” over Philadelphia. Even before the end of 1994, the unification process was already in trouble. Lawsuits were filed. Blackburn says the final straw came when the governor of New Jersey ordered the board to kill attempts to woo a shipping line that was looking for an alternative to the Port of New York.

“We can’t have the future of the Port of Philadelphia under the veto power of a governor who has another port to be concerned about,” Blackburn says.

Officials in New Jersey were more diplomatic. “It’s not easy to get one state to agree on what they want to do, let alone two states,” says Kevin Castagnola, executive director of the South Jersey Port Corporation. “I’m sure somewhere along the line both parties had something to do with [the breakup].”

Regardless of who was at fault, the agency broke apart completely in 1998, just in time for Pennsylvania and New Jersey to begin fighting over the proposed dredging project.

The 2008 Economy League study still identified inter-port conflict as one of the biggest obstacles for the region’s ports. Although Blackburn says that critiques of hostile competition were “exaggerated,” he acknowledges that, in his opinion, hopes of reviving a combined port concept were “hopeless.”

It is small consolation that these problems are not unique to the Delaware Valley. Industry analyst Stephen Fitzroy, senior vice president for Economic Development Research Group, says that Savannah, Ga. and Charleston, S.C. have had similar battles over the future of a common waterway.

The two nearby competitors made an earnest attempt to collaborate, attempting to form a single, combined deepwater port in Jasper County, S.C., a place more naturally suited to freighter traffic. Talks fell apart over issues of jurisdiction and financing, after millions in planning dollars had already been spent. The timeline for the project has been moved decades into the future.

Fitzroy says it was a problem of shifting political will. “They compete, but they also require common access to resources, such as the rivers and channels that provide access to ports,” he says. “They have at various times cooperated and at various times not cooperated, depending on who’s in charge.”

Tomer says the result is more waste as Savannah and Charleston now invest in separate projects to accommodate larger ships. “All of a sudden you went from pooling your resources to competing against one another for the same pot of resources,” he says.

“It’s not easy to get one state to agree on what they want to do, let alone two states.”

Tomer points to one port, Miami, as an example of a smart, cohesive expansion project. It consists of three main site improvements, not dissimilar to those being undertaken elsewhere: Improved rail connections, a tunnel to channel freight trucks away from downtown Miami and speed access to the highway, and a dredging project. But Miami has received a high level of partnership from the state, and sought private partnership for infrastructure improvements to mitigate costs to the public.

Kevin Lynskey, an assistant director at the Port of Miami, says Florida’s top-down system is part of the reason it has received the largest single share of federal TIGER grants for expansion. “At the state level there is a system in place that ensures that there is an equitable distribution of state funding, tending to be given in proportion to the overall size of the port,” he says.

Lynskey says Miami was also uniquely poised to capture more regional shipping for the Florida area, which saw 62 percent of containers come from the West Coast. Its port is close to the ocean, with a seabed comprised of limestone that can be dredged quickly and easily, and requires less maintenance.

“Our investment is relatively modest in terms of deep dredging,” Lynskey says. “Every 10 years we might spend a million dollars to maintain the channel.” The lengthier and silt-filled Delaware currently costs $7 million a year to maintain, a figure that is projected to rise to $8 or $9 million after deepening is completed.

Tomer says these factors made for a smarter investment. “Irrespective of what happens with the Panama Canal, the Miami metro area will be more competitive than the freight and logistics arena on it’s own,” he says.

Fitzroy says Miami is an example of what happens when a port has no nearby states to compete with. “It’s because you’re not talking about the very narrow market within which they’re competing, you’re talking about a level of geography where cooperation benefits everybody.”

While banishing Philadelphia’s rival states is impossible, cooperation is not. Competition may be perfectly healthy in the private market, but it is clear that open strife between quasi-public port agencies only jeopardizes time and infrastructure funding. Looking at Florida, the benefits of cohesion are obvious, and this only makes the Delaware Valley ports’ tacit decision to bleed resources, rather than negotiate peace, all the more troubling. The country continues to indebt itself, and the next time ports begin verging on obsolescence, there may not be the same guarantee that federal dollars will be able to make up for wasteful infighting.

But it is also possible that Philadelphia port officials’ bullishness on their economic future, and their confidence in their ability to best their competitors, will be justified by returns in the still-cloudy future of global shipping.

During Blackburn’s presentation, he mentioned “Southport West” several times, referring to a chunk of brownfield the port authority was able to acquire through riparian rights from the neighboring Navy Yard. The Yard was shuttered in the ’90s and reimagined, with state assistance, as a tax-free office park. It has been wildly successful, now employing more people than when the base was still operational. Old naval buildings now host the headquarters of companies like Urban Outfitters and Tasty Baking in the shadow of glistening new office and hotel complexes.

While the Navy Yard fills in its remaining acreage, Southport West is vacant and waiting. Blackburn says that maybe one day it could hold a distribution center for a company like Walmart or Amazon. Maybe.

Our features are made possible with generous support from The Ford Foundation.

_200_200_80_c1.jpg)

Ryan Briggs is an investigative reporter based in Philadelphia. He has contributed to the Philadelphia Inquirer, WHYY, the Philadelphia City Paper, Philadelphia Magazine and Hidden City.

Next City is a nonprofit news organization that believes journalists have the power to amplify solutions and spread workable ideas from one city to the next city. Our mission is to inspire greater economic, environmental, and social justice in cities.

Learn more about us →

20th Anniversary Solutions of the Year magazine